Dividend notes: reassuring updates - PAG, GHH

I review the latest results from buy-to-let specialist Paragon Banking and optical engineers Gooch & Housego.

In today's dividend notes I discuss reassuring-sounding updates from two very different companies.

Companies covered:

- Paragon Banking (LON:PAG) - a reassuring set of results showing strong performance in the group's core BTL and SME finance markets. Still some macro risk, but I think PAG could be worth considering at current levels.

- Gooch & Housego (LON:GHH) - today's half-year results suggest to me that this optical specialist is getting back on track after a difficult period. I think the shares could prove to be good value at current levels.

These notes contain a review of my thoughts on recent results from UK dividend shares in my investable universe. In general, these are dividend shares that may appear in my screening results at some point.

As always, my comments represent my view only and are not advice or recommendations.

Paragon Banking (PAG)

“We are delighted to deliver another strong financial and operational performance, achieving record interim operating profits, alongside robust growth in our loan book."

Specialist lender Paragon provides buy-to-let mortgage lending and loans for SME business customers. The FTSE 250 group's latest results sent the shares up c.8%, suggesting that the numbers calmed investor fears that the bank could face either a sharp rise in bad debts or a slump in new lending.

The numbers certainly seem fairly positive to me. The bank's underlying profit rose by 22.2% to £128.98m, lifting underlying earnings by 28% to 42.5p per share.

This increase was driven by growth in lending and more competitive funding costs. Total new lending rose by 6.9% to £1.59bn, taking the total loan book to £14.6bn.

This growth was mostly driven by a £1.0bn (19%) increase in mortgage lending. Of this, 98.6% went to professional landlords, underlining the group's focus on this sector. While Paragon does have some residential mortgages in its portfolio, these are in run-off mode.

Funding costs for new loans benefited from higher interest rates. These allowed Paragon to attract an additional £2bn of cash from savers. Total deposits rose by 20% to £11.9bn.

Profitability: Deposit funding can be one of the cheapest ways for banks to fund their lending. Paragon says its funding costs are now "sub-SONIA" – in other words, below wholesale interbank rates. (SONIA is the replacement for scandal-hit LIBOR.)

As a result, Paragon's net interest margin rose to 2.95% during the half year (H1 2022: 2.57%). The bank now expects to report a figure of c.3% for the full year.

Underlying return on tangible equity of 18.7% for the half year (H1 2022: 15.5%). Management expect a figure above 15% for the full year.

Balance sheet & impairments: Paragon's CET1 ratio remains very healthy at 15.6%, although that's down slightly from 16.3% at the end of the last financial year in September 2022.

Arrears remain low, though. Additional impairment charges totalled just £7.5m during the half year and total provisions across the group's loan book remain low at £68m (H1 2022: £55.2m).

The bank ended the period with net tangible assets of 535p per share, broadly in line with the share price at the time of writing.

Dividend: the interim dividend was increased by 17% to 11p, putting the bank on track for a full-year payout of 33p, based on consensus estimates. That's equivalent to a 6% yield at current levels.

An additional £50m share buyback was also announced, taking the total underway to £100m.

Outlook: guidance of new mortgage lending and margins have been edged up slightly, but there are no significant changes. Broker forecast put Paragon shares on a P/E of 6 with a yield of 6%. That could be cheap if this level of profitability can be maintained.

My view: these results contain some isolated signs of weaker conditions in both commercial and residential property markets. The mortgage lending pipeline is down and redemption rates have risen slightly.

Commercial property development lending has slowed dramatically.

However, credit quality remains good and Paragon looks in good financial shape to me. I think things would have to get significantly worse for a dividend cut to be needed.

I don't have any insight into the economic outlook, but if predictions of a relatively minor slowdown are correct, I think Paragon could be a decent buy at current levels.

Gooch & Housego (GHH)

"Full year expectations are unchanged"

This industrial group is a specialist in photonic engineering – the group produces specialist opticial components and systems. Markets include industrial lasers, semiconductor manufacturing, defence, healthcare and aerospace.

It's a highly-specialised business with a long pedigree – the group was founded in 1948 and has been listed on the London market since 1997.

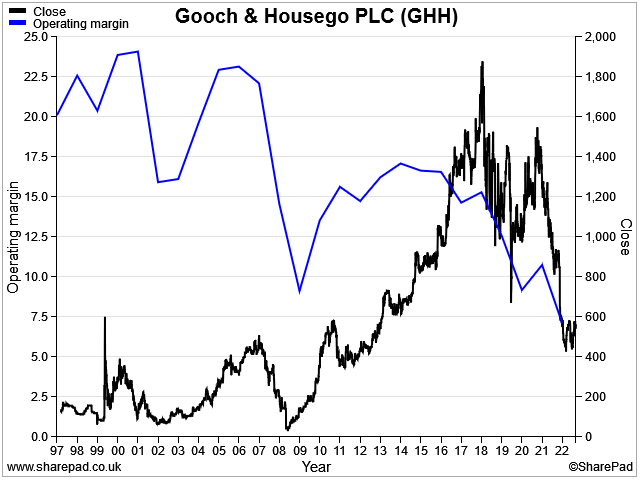

Unfortunately progress has stalled in recent years, with a sharp reduction in profitability. This culminated in a profit warning last August that's left the stock trading at 10-year lows.

Today's results reiterate full-year expectations and suggest to me that the business could be getting back on track.

Financial highlights: revenue for the half year rose by 31.7% to £71.3m, while adjusted pre-tax profit was 26% higher, at £4.5m.

Cash flow from operations rose by c.50% to £6m despite increased inventories, allowing free cash flow to turn positive by c.£1m.

Although net financial debt rose by £7m to £12.9m duing the half year, I don't see any serious concerns here. The impression I get from the accounts is that the performance of the business is recovering and it remains in sound financial health.

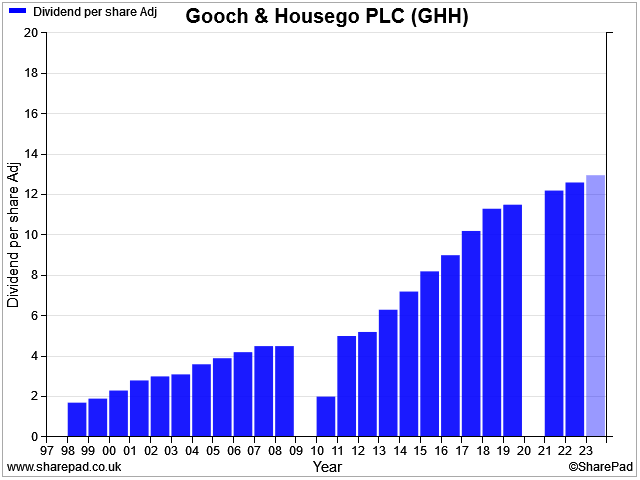

The interim dividend rose by 0.1p to 4.8p per share. That puts the group on track for a payout of 13p this year, resuming a 25-year growth trend:

Operational summary: Gooch & Housego saw "record levels of order intake" during the second half of last year, but this wasn't unvarnished good news. The surge in orders was caused by customers "overdriving their supply chains" to try and offset supply problems and get ahead of price inflation.

As a result, GHH was left with an order book it couldn't fulfil in a timely way. Production rates have increased and the company says that lead times are now coming back to more normal levels.

After some initial difficulty, the company appears to be negotiating this situation successfully, albeit with some after effects.

One problem is that after panic-buying last year, some of the company's customers are now scaling back their ordering. The firm says its book-to-bill ratio fell to 0.8x during the first half of this year. The value of the order book fell from £148m in September 2022 to £124m at the end of March.

The other challenge I can see is that Gooch & Housego is having to absorb some cost inflation on orders booked last year. The company has passed on wage increases to its staff and accepted higher raw material costs. But GHH's own price increases are only being implemented with a lag – presumably this is because they can't be applied retrospectively to the order backlog.

This could result in a surge in profitability next year, assuming new order levels remain healthy. But it's a point worth monitoring in the meantime, I think.

Outlook: management say that the current order book is sufficient to underwrite full-year expectations, which are unchanged.

Broker forecasts suggest earnings of 29.2p per share for the year ending 30 September 2023. That puts the stock on a forecast P/E of 20, but this multiple is expected to fall to 15 in FY24 as margins recover and growth resumes.

My view: I think there's still some uncertainty about the trajectory of the order book over the next 18 months. But my impression from today's results is that the company is back on track and doing all the right things.

I think it's reasonable to expect a steady recovery in margins and profits over the next couple of years.

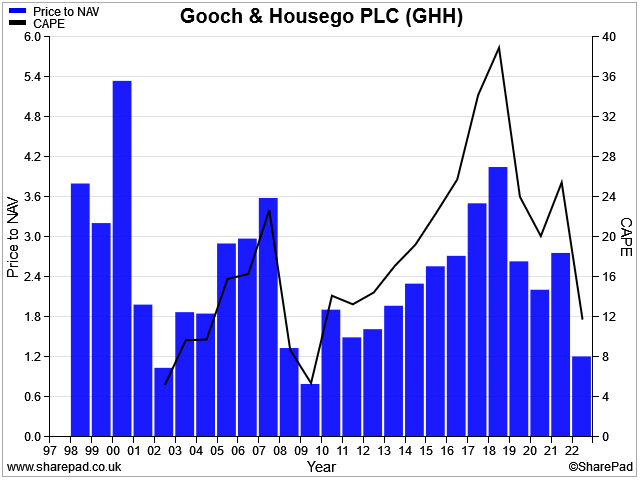

As such, the shares might not be expensive at current levels. Indeed, SharePad data suggests Gooch & Housego stock is currently trading at its lowest level relative to book value since the 2008 financial crisis:

I think this could be worth further research. On this initial inspection, I'm inclined to think that the shares could offer a buying opportunity at current levels.

Disclaimer: This is a personal blog and I am not a financial adviser. All content is provided for information and educational purposes only. Nothing I say should be interpreted as investing advice or recommendations.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.