New stock: a high-quality SaaS business with sticky customers

This UK software firm provides mission-critical services to enterprise customers. It boasts high margins and has a history of generous special dividends. Here's why I'm adding this company to my dividend portfolio.

When I add a new stock to my dividend portfolio, it's rarely a business that's completely new to me. More often, it's a company that I've followed for some time and gradually learned about. Doing this allows me to gain conviction while waiting for a suitable buying opportunity.

The subject of this new stock review is a case in point. I first wrote about this software business in a Dividend Note in 2024. At the time, I noted its excellent quality metrics, super cash conversion and preference for paying special dividends (no doubt influenced by founder ownership).

It's also a Rule of 40 stock: a software business where revenue growth and the group's EBITDA margin sum to more than 40%. This isn't a concept I place too much weight on, but I do think it's a positive reflection on the profitability and growth potential of this business.

Back in 2024, I concluded that the company might be an interesting investment, but I was unsure about the valuation.

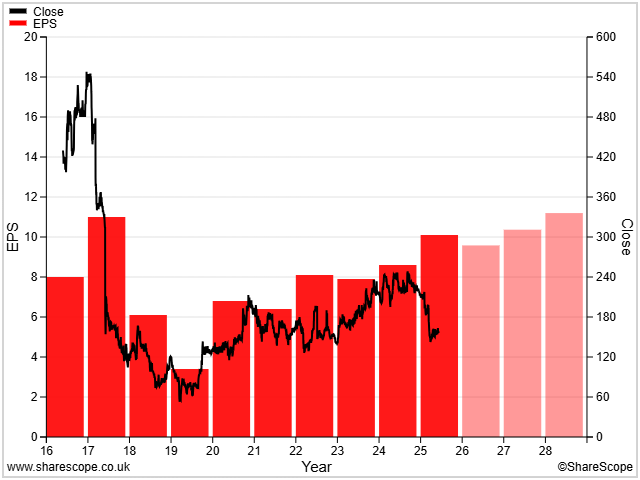

Fast forward two years and the share price has fallen, while earnings have risen.

Indeed, shares in this company now trade at half their 2017 IPO price, despite a substantial increase in sales and profits over the last eight years. The outlook is also fairly positive:

While there have been some company-specific factors at play, my impression is that this year's sell-off has been triggered by the SaaSpocalypse. This sector-wide sell-off has left shares in this business trading on just 16x forward earnings.

In my view, that could be a fairly undemanding valuation for a business with 50%+ returns on equity, extreme customer loyalty and long-term growth prospects.

I've spent some more time learning about this business in recent months. My conclusion is that it could be an interesting choice to consider for the vacant 20th slot in my quality dividend portfolio.

In this review I'm going to take a look at the company in question and run it through my scoring system to see whether it could earn a place in my portfolio.

Disclosure: at the time of publication I do not own shares in the company under discussion.