Nichols: fizzy yield could provide durable income

Vimto-maker Nichols has been in business for over 100 years. This family firm boasts impressive quality metrics and a cash-rich balance sheet. Recent performance suggests the business may be returning to growth after a difficult period.

I'm looking for a dividend stock from the consumer goods sector to replace one of the existing holdings in my model dividend portfolio.

In this share review I'm going to take a look at Nichols (LON:NICL) – the 118-year-old maker of Vimto and other soft drinks. This AIM-listed stock has sales in over 60 countries and uses the same capital-light model favoured by Coca-Cola to generate high returns on capital.

Nichols has fallen out of favour with investors in recent years following a difficult period during the pandemic, when overexposure to out-of-home sales and some sub-par acquisitions contributed to a profit slump.

The company has now addressed many of the issues it faced and results are improving. I don't think the current valuation reflects the quality or value on offer from this 118-year old family business.

I'm also tempted by the recently enhanced dividend policy, which means the shares now boast a forecast yield in excess of 5%.

Disclosure: at the time of publication I do not own shares in Nichols.

Table of Contents

- A family favourite with an international twist

- Recent trading & outlook - expectations unchanged

- Crunching the numbers - how does Nichols score in my ranking system?

- Dividend culture - a proven track record of commitment

- Dividend safety - a well-supported payout

- Dividend growth - I think fundamental support remains strong

- Dividend yield - a more generous payout policy could see the yield top 5%

- Valuation - the shares look cheaper than they have done since 2011

- Profitability - after a difficult patch, quality metrics have bounced back

- Fundamental health - a very strong balance sheet

- Momentum - analysts are optimistic, but the market is not yet convinced

- Conclusion - could Nichols be a suitable addition to my dividend portfolio?

A family favourite with an international twist

In 1908, Manchester herbalist John Nichols invented Vimtonic – a herbal tonic designed to give people 'Vim & Vigour'. Nichols delivered the product to shops, cafes and temperance bars in the local area and it quickly became popular.

The recipe for Vimto – still used today – includes a mix of grape, blackcurrant and raspberry juice, plus a secret combination of herbs and spices.

Vimto rapidly gained popularity and was soon sold in both cordial and carbonated ready-to-drink formats. Steady expansion saw Nichols leverage both the (then) British Empire and the temperance movement to reach a far larger market at home and abroad.

Today, Vimto is a staple of UK supermarket drinks aisles and out-of-home offerings.

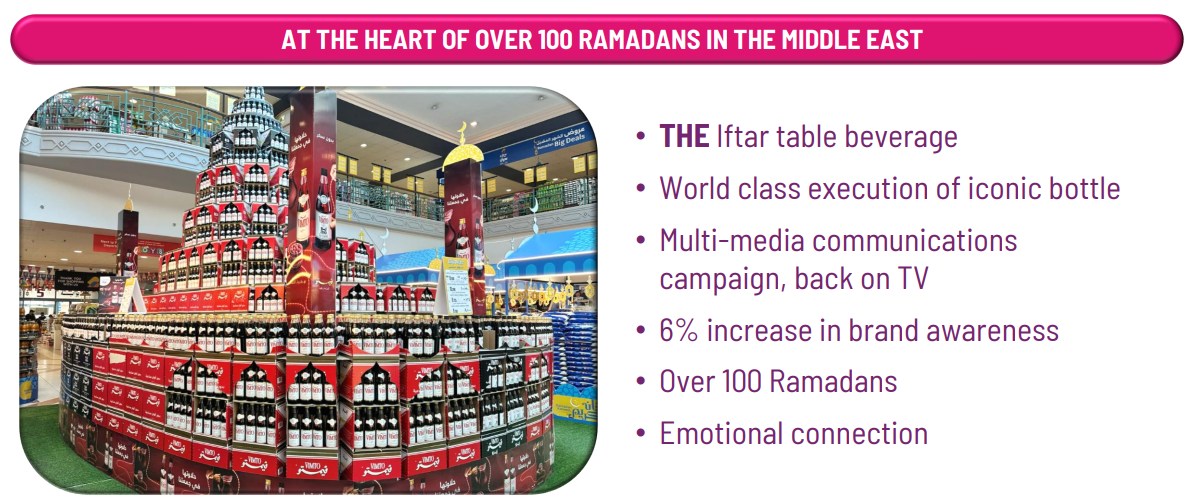

Export sales contributed a quarter of the group's revenue last year and take place across Africa and the Middle East, where Vimto is a staple part of the Iftar evening meal during Ramadan.

Like its much larger rival Coca-Cola, Nichols operates a capital-light model that sees the company sell concentrate syrup to bottlers and licensed partners in each of its geographic markets.

This model supports high returns on capital and a cash-rich balance sheet that's allowed the company to execute a turnaround without any unnecessary financial stress.

A family business? Following the retirement of John Nichols as chairman in 2023, Nichols is no longer led by a family member.

Mr Nichols is the grandson of the company's founder and first joined the company in 1971. He remains on the board as a Family Representative Director, as does his son Matt Nichols, who is also the group's Commercial Director - International.

The Nichols family also retains a sizeable shareholding, suggesting to me that this remains a family-controlled business, like a number of others in my portfolio.

Recent trading & outlook

"Full year expectations remain unchanged with positive trading momentum set to continue as we complete Phase 2 of our concentrate model shift."

2025 full-year results (11/03/26): last year's results showed a welcome improvement in margins, despite limited sales growth:

- Revenue up 1.3% to £175.1m

- Pre-tax profit up 21.5% to £29.2m

- Adjusted earnings up 5.5% to 67.53p per share

- Net cash up 3.8% to £55.7m

- Operating margin: 15.6% (2024: 12.4%)

- Return on capital employed: 27.5% (2024: 24.9%)

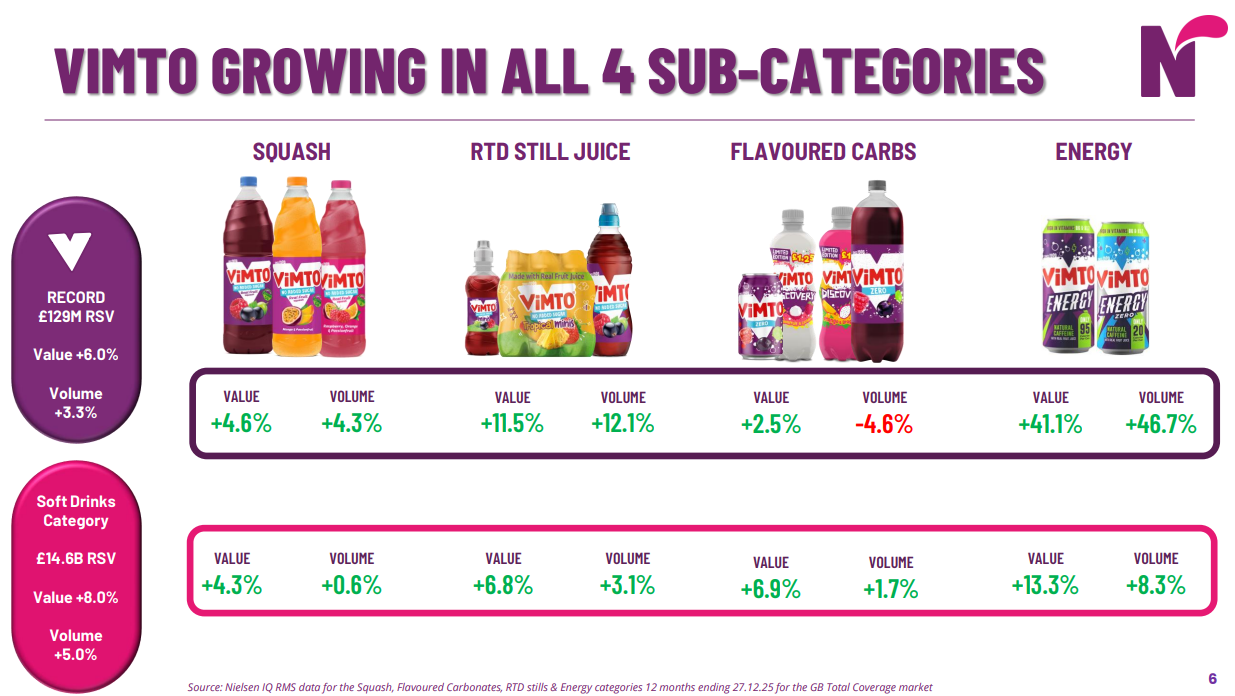

UK: the company reported "sustained growth in UK Packaged" products, with the total retail sales value of products sold rising by 4.8% to £135m. Growth in the core Vimto brand was driven by product innovation and market share gains across newer formats such as ready-to-drink and energy.

Licensed brands such as Levi Roots and Slush PUPPiE are also said to have performed well.

International: export performance was a little mixed due to a variety of factors:

- Middle East: revenue fell by 15.5% to £12.0m, which management says related to the timing of shipments in 2024 and 2025 prior to peak Ramadan demand. Vimto was launched in Yemen and Iraq during the year.

- Africa: like-for-like revenue rose by 9.4%, with total revenue up 5.7% to £20.8m. However, margins improved significantly as the company completed a shift from shipping finished goods to selling concentrate in African markets.

"Our strategy to move can production closer to the point of consumption provides volume, margin and carbon reduction ESG benefits."

- Other international markets: Nichols is focused on building volume in Europe and North America, where market penetration is currently low. These regions contributed £9.2m of revenue last year. In Malaysia, where Vimto launched in 2024, the company focused on securing retail listings (>3,000 stores) and raising awareness through marketing campaigns. As a predominantly Muslim country, Malaysia may offer an opportunity to replicate the Ramadan popularity of Vimto in the Middle East.

Outlook: "Looking ahead, we anticipate delivering another strong performance in 2026 despite ongoing macroeconomic uncertainty. Trading in 2026 to-date has been positive and in line with our expectations."

House broker Singer Capital left its forecasts unchanged at the time of the 2025 results, reflecting uncertainty due to the Middle East conflict:

- FY26E adj EPS: 71.6p (+6.1% vs FY25)

- FY27E adj EPS: 76.6p (+7% vs FY26)

At the time of writing these forecasts put the shares on a FY26 forecast P/E of 13 – not excessive, in my view.

AGM Trading Update (21/04/26): this update left full-year expectations unchanged but did perhaps sound a note of caution:

- Middle East conflict "may lead to some volatility in supply chains and key input costs";

- International sales will be weighted to the second half of the year, due to the timing of concentrate shipments to Africa and the Middle East.

Many companies have highlighted the potential impact on supply chains and cost inflation from the Middle East conflict. However, I think it's worth emphasising Nichols' exposure to this end market, which is unusually high for a UK-listed consumer business.

Nichols: crunching the numbers

Description: a UK soft drink producer that owns the Vimto brand, together with a number of other licensed and owned brands. Sales are concentrated in the UK, Middle East and Africa, although the business is expanding more broadly.

| Nichols (LON:NICL) |

Quality Dividend score: 63/100 | Forecast yield: 5.5% |

| Recent share price: 948p | Market cap: £342m | All data at 21 May 26 |

Latest accounts: 2025 full-year results

In the remainder of this review, I'll step through the different stages in my dividend screening system and explain whether I think Nichols could be a suitable addition to my quality dividend portfolio.

As a reminder, this is a scoring system I've developed to rank shares for the qualities that are important to me, from a quality dividend perspective.

My choice of scoring factors is of course personal and highly subjective. These scores are not intended to be used as a guide on when to buy or sell shares. They're simply one factor I use to assess a stock's potential attractions, in addition to broader, company-specific analysis.

Unless specified otherwise, the financial data I use in this process is drawn from ShareScope.

Dividend culture: a strong commitment

Family-controlled firms are often a good place to look for reliable dividends. Multi-generational family ownership often see dividends as a core part of their income stream and prefer them to share buybacks – a view I share.

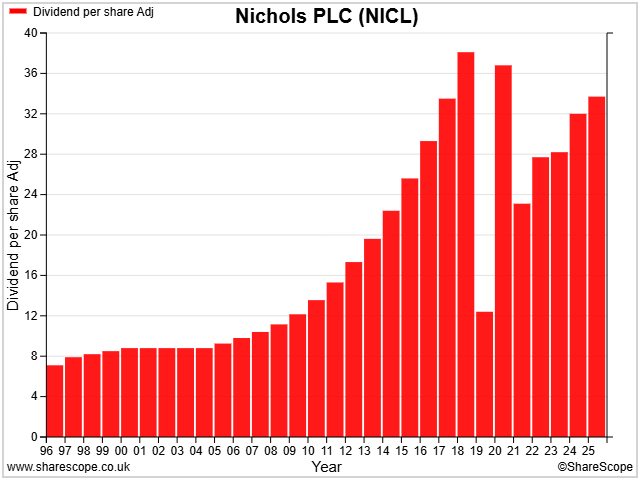

Nichols chose to cut its dividend during the pandemic, when over-exposure to out-of-home (foodservice) sales caused profits to plummet during lockdown. While the group's net cash position was never threatened, the outlook at the time was uncertain.

This cut ended a 30-year run of unbroken dividend growth, but Nichols has maintained annual payouts for the last 34 years, according to ShareScope. The payout is now moving back towards its pre-pandemic levels and last year's return was boosted by an additional special dividend of 54.8p per share.

I am confident that Nichols has a strong dividend culture.

Nichols scores 5/5 for dividend culture in my screening system.

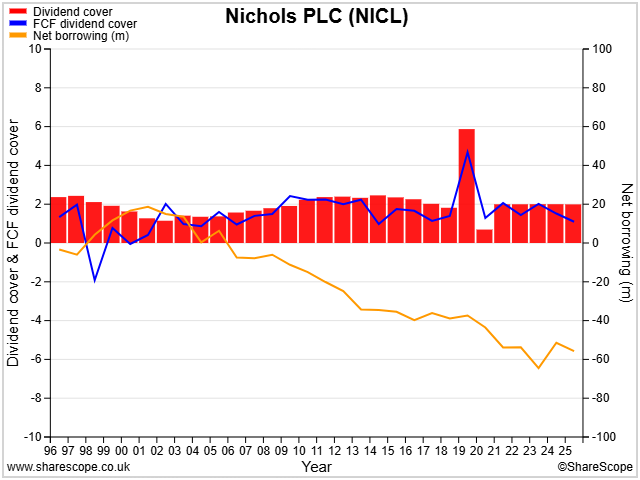

Dividend safety: excellent

My dividend safety scores looks at how well the dividend is covered by earnings and free cash flow. I also take into account a group's net debt (or cash) position.

I have few concerns in this area with Nichols. As the chart below shows, the group has maintained dividend cover in the range of 2x for most of the last 30 years. Free cash flow cover has also been consistently comfortable, while net cash has accumulated.

The only caveat to this is that from 2026, Nichols has altered its dividend policy to target 1.5x cover.

Given the group's £50m+ net cash position I think this should be safe enough – this year's forecast payout of 51.4p per share would cost £18.8m. But changes to longstanding policy are always worth monitoring, so I will be keen to see that free cash flow cover remains healthy.

Nichols scores 4.2/5 for dividend safety in my screening system.

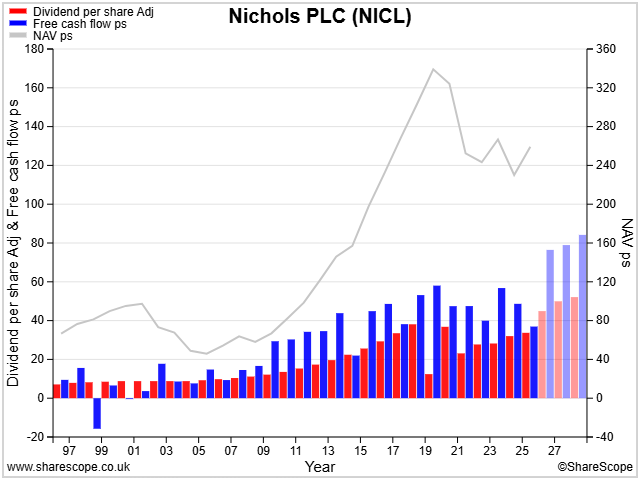

Dividend growth: better than it seems?

My dividend growth score is designed to test the sustainability of a company's payout growth by comparing it to free cash flow and net asset value per share. The logic is that if these two other metrics don't increase in similar proportion to dividend growth, support for the payout is likely to weaken over time.

Nichols' track record prior to the pandemic was excellent. But the company's payout (red bars below) is still slightly below its pre-pandemic peak and both NAV per share and free cash flow have also weakened during the recent turnaround period. This has resulted in Nichols scoring zero in my dividend growth category:

I think this result is probably a little harsh, given the context. Free cash flow cover has remained positive following the reduction to the payout. As I mentioned above, the payout is also expected to rise significantly this year, taking it above its 2019 level.

Broker forecasts suggest free cash flow will also stabilise, delivering cash cover for the dividend of around 1.5-1.6x.

Companies rarely achieve a top score in all categories at once. I'm willing to overlook this shortfall. In my view, Nichols' strong balance sheet and proven dividend culture should underpin sustainable growth over the coming years.

Nichols scores 0/5 for dividend growth in my screening system.

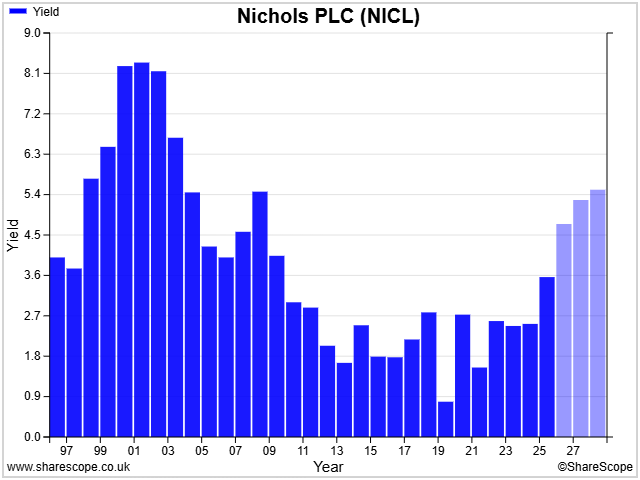

Dividend yield: improving

When scoring a stock for dividend yield I consider the five-year average, trailing yield and forecast yield.

What's clear is that Nichols used to command higher yields in the past, prior to 2010. My view on this is that this correlates to the start of the low interest rate era, where companies with reliable dividends were bid to higher valuations than in the past.

This was a particularly noticeable trend with a number of high quality AIM dividend stocks that were popular with AIM IHT fund managers. Many of these have de-rated since, perhaps partly due to persistent fund outflows. I see this as a potential opportunity.

Nichols scores 2.8/5 for dividend yield in my screening system.

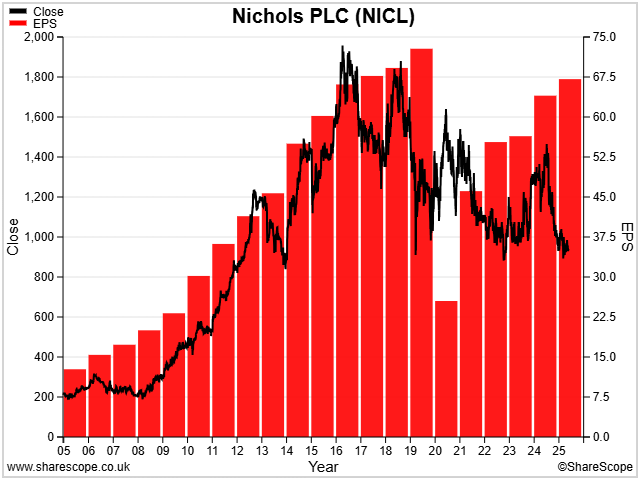

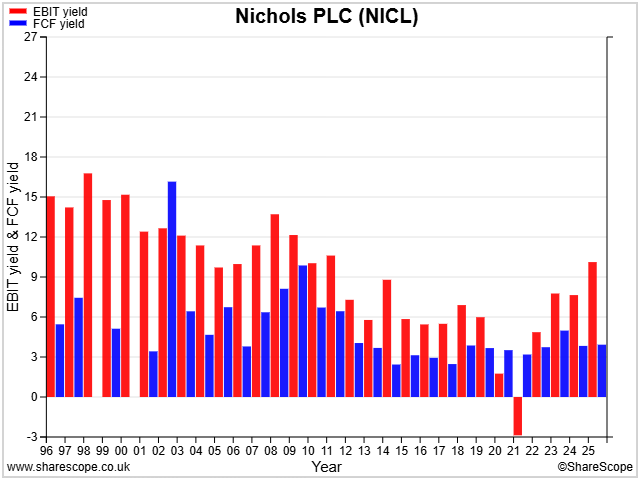

Valuation: relatively cheap

To calculate my screening score, I look at a company's valuation based on its EBIT/EV yield and its free cash flow yield. I see these measures as a more useful guide than the P/E to the valuation of the whole business and the level of sustainable return potentially available to shareholders.

The chart below shows some inconsistency in recent years. But it also highlights how the recovery in profit since 2022 has left the stock looking potentially cheap, with an EBIT yield that's nearing 10%. (As a rule of thumb, I tend to use 8% as a threshold for value.)

The caveat to this is that the company's cash generation also needs to recover. I think it will. Checking last year's cash flow statement shows some large unfavourable working capital movements which the company says resulted from the timing of some year-end sales.

This is expected to unwind during the first half of 2026 and not recur this year. Broker forecasts suggest free cash flow could be c.£30m this year, giving a potential free cash flow yield of more than 8%.

Fair value estimate: various valuation methodologies exist to try and calculate the intrinsic value of a company's shares. I tend to be careful about relying on them too heavily because they require predictions about the future.

Even so, I find fair value estimates useful for providing a different perspective on valuation to the relative valuation ratios I use in my scoring system.

The intrinsic valuation methods I tend to use are earnings power value, the dividend discount model and discounted cash flow.

In Nichols' case, applying a 10% required rate of return and some conservative estimates on long-term growth gives me a range of fair value estimates from c.750p to 1,150p, depending on which method I use.

Averaging these gives me c.910p, slightly below the last-seen share price of 948p. This is perhaps a sign that Nichols isn't necessarily all that cheap unless the business can deliver the hoped-for return to sustainable growth.

Nichols scores 3.5/5 for valuation in my screening system.

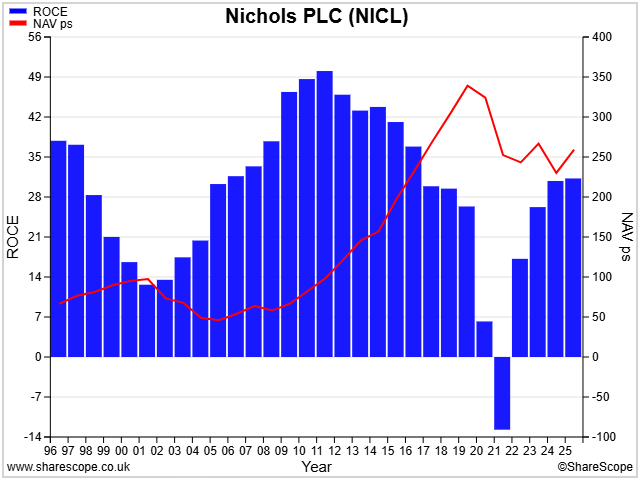

Profitability: fully recovered?

For non-financial stocks I use return on capital employed (ROCE) as my main indicator of profitability, paired with net asset value per share growth.

The reason for this is that a business generating consistent returns on a growing asset base should increase in value over time. I see ROCE as a more useful measure than profit margins for gauging whether a company has the potential to deliver long-term compound growth.

ROCE is not necessarily as useful in the short term, but that's not my main concern for this portfolio.

My screen blends five-year average ROCE, trailing-12-month ROCE and NAVps growth to give an overall score.

Despite last year's excellent ROCE result, two factors combine to suppress my overall profitability score for Nichols:

- Five-year average ROCE remains depressed;

- The group's net asset value is still below its 2019 peak, largely relating to the underperforming out-of-home business.

Nichols scores 3/5 for profitability in my screening system.

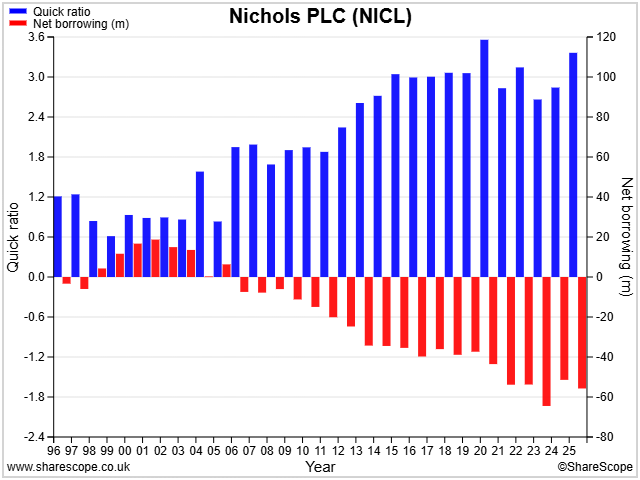

Fundamental health: very strong

My scoring algorithm uses interest cover and net debt to gauge a company's fundamental health. However, Nichols has net cash and net interest income, so these factors aren't very relevant.

To illustrate the company's balance sheet strength, I thought it might be more useful to look at how the company's quick ratio and net cash position have evolved over time.

As a reminder, the quick ratio compares current assets (excluding inventories) with current liabilities: it's a measure of a company's ability to meet its near-term liabilities from liquid assets.

We can see from the chart that Nichols maintains a high level of liquidity:

Indeed, checking last year's balance sheet suggests the company could have settled all of its outstanding payables at the end of the year from net cash, without needing to convert its receivables into cash. That's a strong position to be in.

Nichols scores 5/5 for fundamental health in my screening system.

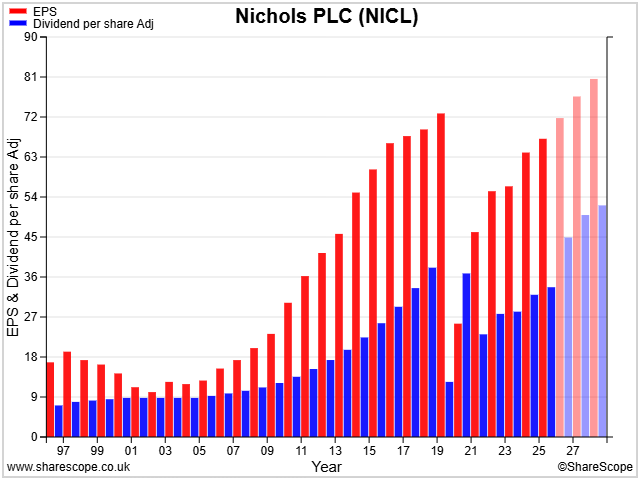

Momentum: middling

The momentum element of my scoring algorithm is a relatively new addition. I discussed it in more depth here.

In short, I look for a pattern of improving earnings (recent and forecast) and some technical share price momentum. I also want to see forecast dividend growth.

We can see from the chart that Nichols earnings and dividend have both returned to growth. Broker forecasts suggest they will continue rising over the next couple of years.

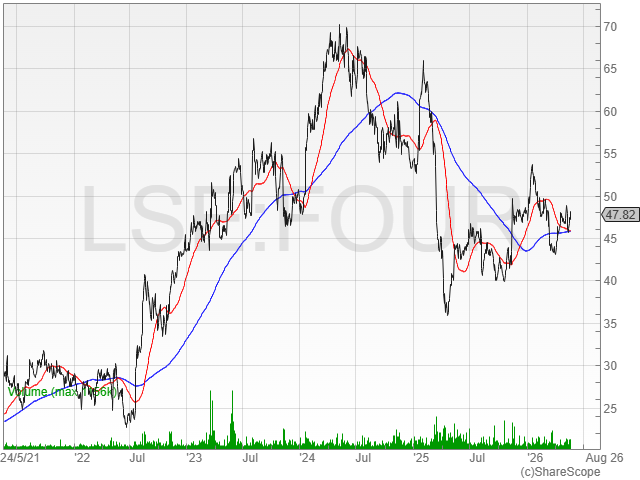

Share price momentum is a little less certain, I think.

I'm no chartist, but the measure I use here to gauge momentum is the ratio of the 50-day moving average (red line) to the 200-day moving average (blue line).

This is a commonly used charting approach to gauge the medium-term trend of a stock. Ideally, the 50dMA would be comfortably above the 200dMA, indicating positive share price momentum.

In this case, the two lines are both at the same level, perhaps indicating somewhat uncertain momentum:

My hope with Nichols is that if earnings follow forecasts, buyers will gradually return to the stock when it becomes too cheap to ignore.

Whether this transpires remains to be seen, of course – my momentum score is still new and has not yet had chance to prove its worth.

Nichols scores 2.5/5 for momentum in my screening system.

Conclusion: a definite contender

My dividend screening system awards Nichols an overall score of 62/100 at the time of writing (May 2026).

I covered Nichols briefly in a dividend note in March 2024 and have followed it in the background for several years. It's a defensive consumer goods business with the kind of characteristics that have historically supported reliable dividend growth over long periods.

The past is no guarantee of the future, of course. Nichols lack of family management could see the company lose its focus, while its niche brand – albeit a large niche – could eventually reach growth limits as fashions and tastes change. Ultimately, this is a business that sells sugary drinks, after all.

Despite these concerns, I think the valuation, balance sheet and trading outlook all point to a potential opportunity – if the company can avoid further missteps.

Roland Head

Disclaimer

This is a personal blog/newsletter and I am not a financial adviser. All content is provided for information and educational purposes only. Nothing I say should be interpreted as investing advice or recommendations.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.