Dividend notes: a super small cap? XPS, SDY

23/06/23: I review this week's results from advisory group XPS Pensions and consider the 8% yield on offer at equipment firm Speedy Hire.

Welcome back to my dividend notes. In this piece I'm catching up on a few small-cap results from earlier this week.

Companies covered:

- XPS Pensions (LON:XPS) - a solid set of numbers from this pensions advisory and administration business. Shares offer a useful 4.8% dividend yield and I think this stock could become a reliable source of income.

- Speedy Hire (LON:SDY) - last year's results show strong revenue growth, but falling margins and poor capital allocation, in my view. The near-8% dividend yield looks a little risky to me. I think there are better choices elsewhere in this sector.

These notes contain a review of my thoughts on recent results from UK dividend shares in my investable universe. In general, these are dividend shares that may appear in my screening results at some point.

As always, my comments represent my view only and are not advice or recommendations.

XPS Pensions (XPS)

"We remain confident in delivering against our expectations for the current year."

This specialist pensions advisory and administration group is a new business for me, but my initial impressions are that it could have decent potential as a dividend share.

To start building up my understanding of XPS, I've decided to take a look at this week's full-year results and note down some thoughts here.

What does it do? XPS appears to offer a wide range of pension-related services, including consultancy and adminstration. This is a complex area given the level of regulation involved and the many and varied pension funds that exist in the UK.

XPS also appears to be a fund manager, in a small way. The group runs the National Pension Trust. This has £1.4bn of assets under management and is a DC Master Trust.

A master trust allows companies to consolidate their DC pension schemes into the master trust, effectively outsourcing it.

Results summary: these results cover the year to 31 March 2023 and represent the sixth consecutive year of growth since the company listed in 2017.

The numbers do seem quite strong to me, with revenue up 20% to £166.6m and operating also up 20%, to £22.7m.

(I'm using the reported profits here. XPS appears to be quite a heavy adjuster, but having looked at the adjusting items my view is that most can fairly be described as regular operating costs – e.g. share-based payments to staff. So I've included them all. That's my choice - others may take a different view.)

Cash generation appears to be pretty strong. My sums suggest free cash flow of £20.6m last year (FY22: £11.7m). This gives a free cash flow yield of 5.7% and represents cash conversion of 130% from after-tax profit. In FY22, the equivalent cash conversion ratio was 125%. Strong numbers.

Profitability was fairly good, although not quite as high as I thought it might be. My sums show an operating margin of 13.6% (FY22: 13.7%) and a return on capital employed of 9.4%. Okay, but not outstanding.

Operating summary: management report strong year-on-year growth in Pensions Actuarial Consulting (+24% YoY) and Investment Consulting (+31% YoY).

Growth in pensions administration was respectable, at +10% YoY.

XPS says that its business is non-cyclical and is continuing to expand into "higher margin" growth areas such as Risk Transfer and DC Consulting. I agree that these seem likely to remain important markets over the coming years.

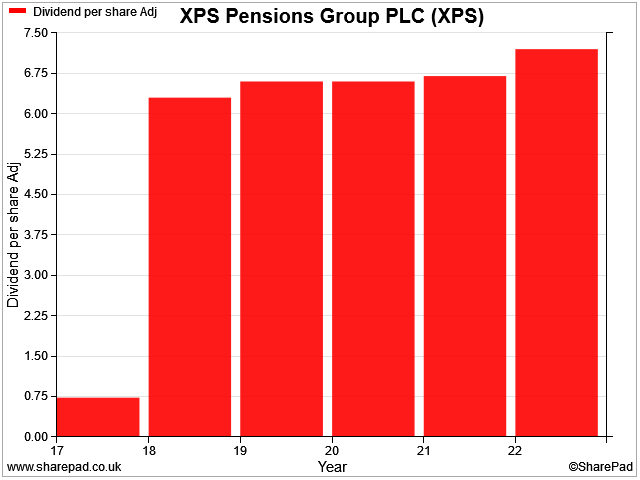

Dividend: shareholders will receive a full-year payout of 8.4p per share.

This payout gives the stock a yield of 4.8% at current levels and represents 85% of free cash flow, by my calculation. That looks reasonably affordable to me in the context, albeit not bulletproof.

XPS has paid steadily increasing dividends since its 2018 IPO, backed by free cash flow. If this record can be maintained, I think it could become an interesting income stock.

Outlook: management believes that with market share still under 10%, XPS has "continued opportunities to grow, supported by both market and regulatory tailwinds".

"We remain confident in delivering against our expectations for the current year."

Broker consensus forecasts I can see suggest adjusted earnings will be broadly flat this year, at 12.7p per share (vs. 12.6p in FY23), with a dividend of 8.6p.

These estimates price the stock on 14x FY24 forecast earnings, with a prospective yield of 4.9%.

My view: XPS looks like a decent business to me with the potential to become an attractive dividend stock.

Profitability looks respectable to me and is improving, but it's not quite as wonderful as I might have expected. However, I can see the potential for margins to improve as the business continues to grow.

Right now, the valuation looks fair to me, given forecasts for limited growth this year. But I'm definitely going to start following XPS more closely.

Speedy Hire (SDY)

"Recent key contract wins and extensions, as well as strong pipeline, gives confidence in meeting our expectations for the coming year"

What do you call an equipment hire company that loses £20.4m of "non-itemised assets"? Speedy Hire, in this case.

This embarrassing mishap now appears to have been resolved and the group has a new finance boss. But this episode doesn't seem like a ringing endorsement of the company's management or internal culture, to me.

Notwithstanding this, Speedy Hire's full-year results this week did showcase a fairly respectable performance.

This is the second equipment hire company I've covered recently – the first was VP, last week. Suffice to say there is a substantial contrast between the two.

Financial summary: revenue rose by 13.9% to £440.6m during the year to 31 March, with adjusted pre-tax profit up 6.6% to £32.1m. Free cash flow managed to turn positive, rising to £10.6m (FY22 saw an £18.5m outflow).

When revenue growth is greater than profit growth we know that margins have fallen. That's the case here. Excluding the impact of the £20.4m asset write-off, I estimate that Speedy Hire generated an operating margin of 7.0% last year, compared to 9.0% the previous year.

Return on capital was 8.5%. I'd guess this is unlikely to be much above the group's cost of capital. Given this, I'm unimpressed by management's decision to use £24m of debt to buyback shares last year.

This resulted in a £25m increase in net debt to £92.4m, adding risk without doing anything to make the business more productive or profitable.

Although Speedy's net debt is still less than half the £208m book value of the hire fleet (my rule of thumb for this sector), I think buybacks are a rash use of money for a low-margin business whose £70m depreciation charge suggests it needs to replace a third of its fleet every year.

I think shareholder returns would be better served by deleveraging and improving the performance of the business. It's also worth noting that most of these shares were probably repurchased at levels above the current share price – not ideal:

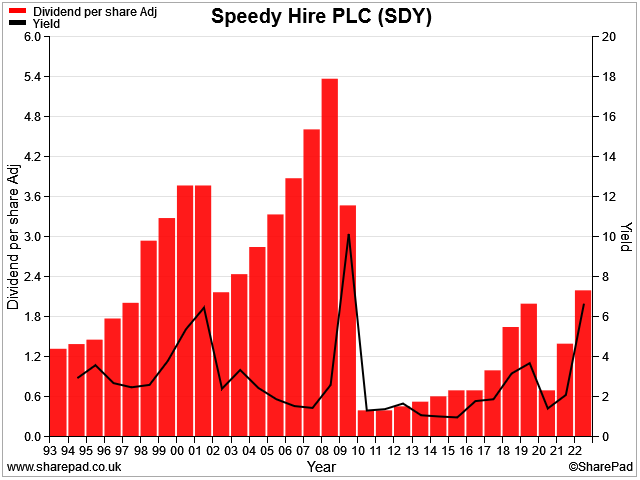

Dividend: the full-year dividend has been increased by 18% to 2.6p per share. This provides a tempting 7.8% yield at current levels.

However, my sums suggest this payout will cost £12m, swallowing up all of last year's free cash flow and then a little more.

I can't see the justification for such a big increase in the payout, given the group's debt level, poor cash conversion, and falling profit margins.

Speedy Hire is the third company I've covered this week (following Halfords and DS Smith) that appears to be trying to placate shareholders whose stock has fallen by offering bumper payouts.

Outlook: recent contract wins and a strong pipeline "give confidence", but CEO Dan Evans also warns of the "continuing challenges of the macro-economic climate".

In its year-end trading update in April, Speedy said it had seen "some softening of demand in recent weeks". This comment wasn't repeated in the full year results. Have market conditions stabilised?

Broker forecasts suggest a fairly flat year, with adjusted earnings unchanged at 5.2p per share. That prices the shares on a forecast P/E of 6.

My view: if market conditions remain stable and Speedy Hire can maintain or improve the utilisation of its fleet (which fell from 57% to 54% last year), then I can see the shares could offer attractive value and yield at current levels.

Personally, I'm not tempted. I don't think Speedy Hire is a high quality business and I certainly don't see it as a quality dividend stock, despite the high yield.

The company's dividend history provides what a reminder of the cyclical risk in this business. When Speedy Hire's dividend yield has peaked at this level previously, the omens have not been positive:

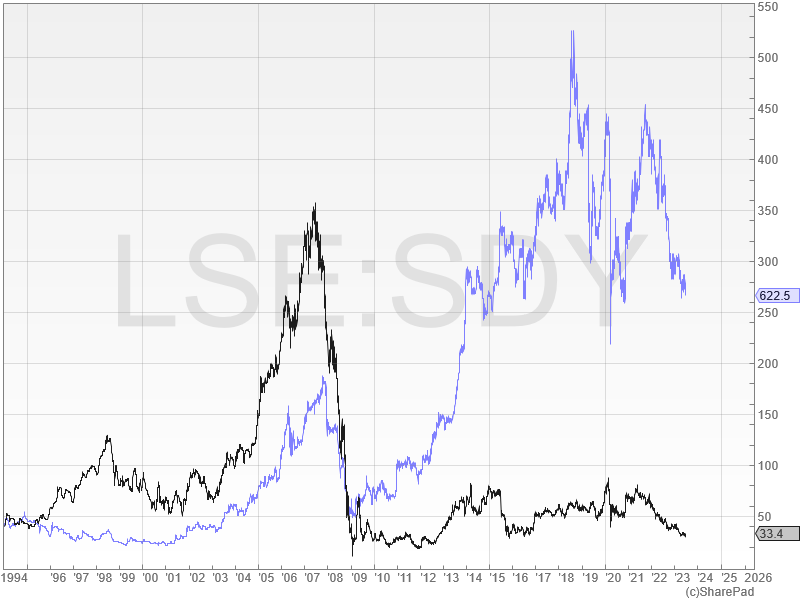

If I wanted to invest in this sector I would buy shares in VP. I think this owner-managed business is of much higher quality and benefits from stronger management.

The two companies' performance over the last 30 years certainly suggests that VP has been more successful at creating value for investors:

Disclaimer: This is a personal blog and I am not a financial adviser. All content is provided for information and educational purposes only. Nothing I say should be interpreted as investing advice or recommendations.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.