Dividend notes: upgrade + an 8% dividend yield? STEM, NXT, NESF

20/06/2023: updates from Next, SThree and NextEnergy Solar Fund sound confident, but I think some risks remain.

Today I'm covering results from three very different businesses that on my dividend share radar at the moment.

I think there could be some opportunities here, but risks remain.

Companies covered:

- SThree (LON:STEM) - this recruiter reports a small drop in H1 fee income but has plenty of cash and still appears to be robustly profitable. The dividend looks safe to me and I suspect the shares could offer value.

- Next (LON:NXT) - the retailer has upgraded its profit guidance after a strong May. But management don't expect this rate of improvement to last and still expect profits to fall this year. The shares look fairly priced to me.

- NextEnergy Solar Fund (LON:NESF) - the renewables investor has issued bullish guidance for an 11% dividend increase in the 2023/24 financial year, suggesting a potential yield of 8.4%. However, I can see some risks, too. I'll watch with interest but won't be investing at this time.

These notes contain a review of my thoughts on recent results from UK dividend shares in my investable universe. In general, these are dividend shares that may appear in my screening results at some point.

As always, my comments represent my view only and are not advice or recommendations.

SThree (STEM)

"Strong balance sheet, with £72 million net cash as at 31 May 2023 (31 May 2022: £48 million)"

Recruiters are highly cyclical but can deliver high returns and strong cash generation when times are good.

STEM (Science, Technology, Engineering, Mathematics) specialist SThree is a regular presence in my dividend screening results, as is small-cap peer Robert Walters (RWA), which recently issued a profit warning.

I'm not too concerned about the warning at Robert Walters; on a medium-term view. I think the most of the bad news is probably priced in. But when I saw a trading update from SThree a few days later, I did wonder if it would also include a profit warning.

It didn't. The good news for SThree shareholders is that trading during the first half of this year appears to have been in line with broker expectations. However, like most of this sector, SThree shares have already sold off heavily. Is there an opportunity here?

H1 highlights: SThree says that group net fees fell by 2% to £208.6m compared to the same period last year. However, net fees from contract positions were 3% higher at £170.0m, and now represent 81% of group net fees (H1 FY22: 77%).

Permanent net fees fell by 19% to £38.6m, reflecting tough conditions in Life Sciences and the company's deliberate focus on contract revenue in some markets.

Life Sciences appears to have been a weak point – fee income rose in other key sectors:

- Technology: +1%

- Engineering: +17%

- Life Sciences: -21%

Geographically, conditions varied significantly across SThree's three largest markets, which together represent 73% of net fees:

- Netherlands: +3%

- Germany: -1%

- USA: -11%

Overall, the contractor order book is said to be unchanged from the same period last year, as "robust extensions" offset weaker new placement activity. This suggests to me that we're seeing a degree of slowdown in end markets, but not yet a full-blown recession (when contract workforces are often slashed).

Balance sheet: net cash has risen from £65.4m at the end of the financial year (30 Nov 22) to £72m at the end of May.

This cash pile represents almost 15% of the current market cap, so should provide some margin of safety if market conditions worsen. While the cash position remains strong, I suspect the dividend should also remain safe.

Outlook: there's no formal outlook statement in this half-year update, but the commentary strikes a mixed tone.

While chief exec Timo Lehne remains confident about "the structural megatrends" driving STEM growth, he says the business will remain "reponsive to the macro backdrop and how that plays out" on recruitment demand.

An updated (paid) research note from Radnor Capital today (available on Research Tree) leaves forecasts unchanged. Radnor's analysts suggest earnings of 41.3p and a dividend of 16.5p per share for the year ending 30 November 2022.

That puts SThree on nine times forecast earnings, with a dividend yield of 4.5%

My view: I don't know how market conditions will play out, but I can't imagine any realistic scenario where demand for STEM expertise will not remain strong over the next decade.

Broker forecasts for this year show SThree's dividend being covered twice by earnings and backed by more than 50p per share of net cash.

My feeling is that the stock is probably reasonably valued on a cyclical view. I would guess that the shares could do reasonably well from current levels over time, with the caveat that things might get worse before they started to improve.

Next (NXT)

"Trading in the last seven weeks has been materially better than the guidance we issued in May and we are updating the market accordingly."

Retailer Next issued an unscheduled trading update this week, after upgrading its profit guidance for the year.

I last commented on Next in May, when I noted that the company had left its full-year guidance unchanged and pointed out that profits were expected to fall this year. At the time, I suggested that the share price was up with events.

This week's update alters the picture slightly and provides some useful context on UK consumer behaviour, thanks to Next's excellent reporting. So I think it's worth taking a look.

Next says that full-price sales during the first seven weeks of the second quarter have been 9.3% higher than the same period last year. The company's previous guidance was for a fall over 5% over this period.

Management believe there are two reasons for this outperformance:

- Better weather: the warm weathe is thought to have triggered additional sales after "a wet and cold April"

- Annual pay rises: annual inflation was running at 8.7% in April but monthly inflation was 1.2%, according to ONS data. Next points out that if an individual received a 5% annual pay rise in April, their real income would rise by 3.8% in that month:

"We do not think it is a coincidence that sales stepped forward so markedly at a time of year when many organisations make their annual pay awards."

Updated outlook: Next point out that the initial impact of pay rises is likely to fade fast if inlation remains high:

"This is why we are not anticipating the current performance to continue at the same level going forward"

However, £93m of additional full price sales have already been achieved. This has given management sufficient confidence to upgrade full-year sales and profit guidance:

"We are upgrading our full price sales guidance for the full year by £137m and our full year profit guidance by £40m to £835m."

This table shows the impact of these changes on expected performance versus last year:

We can see that full price sales are now expected to rise slightly this year, versus previous guidance for a small fall. (Full price sales is an adjusted measure that excludes some revenue, but it's fine for our purposes here.)

However, adjusted pre-tax profit is still expected to fall this year, albeit by 4% rather than 8.7%. (For context, Next reported pre-tax profit of £870m last year and £823m the previous year.)

The company hasn't provided any updated earnings per share guidance, but consensus forecasts I can see suggest a figure of 518p per share. That's an increase from 505p previously, but still around 10% below the previous year's figure of 573p per share.

Dividend guidance for an ordinary dividend of 206p appear to be unchanged. This payout forms the base element of the company's annual shareholder returns and is typically supplemented by a special dividend or share buybacks.

Based on these estimates, Next shares are trading on about 13x forecast earnings, with a 3% dividend yield.

My view: this week's update doesn't really change my view on Next. The company enjoyed a post-pandemic profit boost last year as consumers caught up on spending.

I don't think the current valuation is unreasonable, and I'm confident the dividend remains safe. But although I think this is an excellent business, I reckon growth is likely to remain challenging.

Next shares have proved to be a good investment for buyers who have taken advantage of periodic sell offs.

I plan to wait for the next such opportunity before considering whether to buy the shares.

NextEnergy Solar Fund (NESF)

"Portfolio continues to outperform, 11% dividend target increase, well placed to deliver shareholders attractive, inflation-protected income"

Results this week from this solar energy fund caught my eye as after recent falls, NESF shares now offer a dividend yield close to 8%.

This isn't an in-depth look at these results. I don't have the time or the sector knowledge to probe too deeply. But I have noted down some factors that seem interesting to me and – in my view – may reflect the mix of risk and possible reward on offer here.

About NESF: this investment company has a £1.1bn of renewable energy assets, predominantly UK solar farms. In total, NESF has 99 operating assets with an installed capacity of 865MW. Last year, they generated 870GWh of electricity.

Results summary: NESF's latest results cover the year to 31 March 2023. Here are some of the main highlights:

- Net asset value up up 1% to £674m

- Net asset value up by 0.8p to 114.3p per share

- Earnings per share of 8.2p (FY22: 21.7p)

- Dividend up 5% to 7.52p per share (FY22: 7.16p)

- Cash dividend cover of 1.4x (FY22: 1.2x)

- Total gearing (inc preference shares): 45% (FY22: 42%)

- Weighted cost of capital: 5.7%

Dividend cover: With this business model, I see cash dividend cover as more important than earnings cover. This is mostly because profits can be heavily affected by non-cash revaluation gains, as with property.

Last year's reported cash dividend of 1.4x seems reassuring. I was curious to see how this cash dividend cover is derived, so I delved into the footnotes.

In short, cash income is calculated by subtracting non-cash factors from revenue. Operating expenses and preference dividends are then subtracted to arrive at a net cash inflow from which dividend cover is calculated. This all seems fine to me.

Net asset value/investment: NESF's inbound cash flows appear to have covered the dividend comfortably last year. But this measure of cover does not reflect cash that flowed out of the business into new investments.

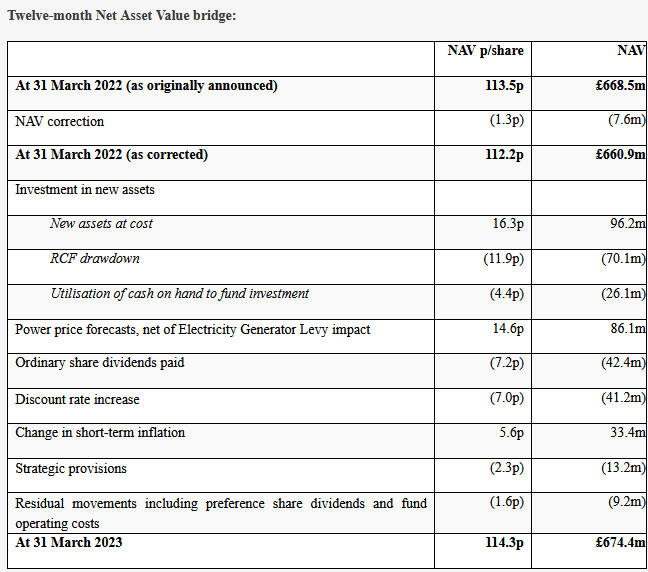

NESF invested £96m in new assets last year, but its net asset value only rose by £13.5m. Intuitively, this seems a smaller increase than I might have expected, given the group's overall gearing of 45%.

Helpfully, the company has provided a breakdown of the factors behind last year's NAV movement. I think this is worth a look, as it highlights the various factors that influence both NAV and future cash generation:

It's worth remembering that net asset value is calculated based on actual and expected cash flows into and out of the business.

Looking at the bridge above tells me that c.73% of investment in new assets last year was funded with debt ("RCF drawdown").

This is considerably higher than the group average leverage of 45% and above the investment policy limit of 50% that applies to the business as a whole. I suspect this explains the recently announced plan to sell 236MW of UK solar assets to reduce RCF drawings.

With the shares trading at a discount to NAV, management believes the market is undervaluing these assets. I have no idea whether this is true, or whether the impact of higher interest rates (reflected in the discount rate increase above) means that these assets are worth less than they might have been previously.

Power price forecasts: what is clear is that NAV would have fallen sharply last year if NESF had not been able to upgrade its power price forecasts to reflect ongoing expectations for higher energy prices.

It's worth remembering that this process may also reverse at some point, if energy prices start to fall.

Outlook: management have taken a bullish stance on the outlook and are guiding for a chunky 11% dividend increase in the 2023/24 financial year. Presumably this is intended to reflect inflation:

"11%dividend target increase to 8.35p per ordinary share for the financial year ending 31 March 2024"

This implies that NESF shares could offer a prospective yield of 8.4% at the last-seen price of 99p.

My view: as I write, NESF shares are trading around 13% below their reported net asset value of 114p.

I think it's possible that this discount is justified by the group's rising leverage and the potential impact of higher interest rates on investment returns.

However, there are a lot of moving parts here that could influence future valuations and cash generation.

I'm going to file this on the too hard pile for now.

I think the 8% yield could offer an opportunity, but not without risk. I'm not interested in buying the shares now, but I will watch developments with interest.

Disclaimer: This is a personal blog and I am not a financial adviser. All content is provided for information and educational purposes only. Nothing I say should be interpreted as investing advice or recommendations.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.