Dividend notes: value or not? BLND, EXPN, BT-A

I review the latest results from a trio of FTSE 100 dividend shares -- British Land, Experian and BT Group. Is there any real value on offer?

Welcome back to my dividend notes. The theme of this post seems to be value – or the lack of it. Let me know what you think.

Companies covered:

- British Land (LON:BLND) - the FTSE 100 REIT has reported a big slump in property values but looks fairly safe and probably cheap, in my view.

- Experian (LON:EXPN) - this financial information specialist delivered a solid if unspectacular performance last year. I like the business, but it's too expensive for me at current levels.

- BT Group (LON:BT-A) - this FTSE 100 stalwart can't stem the cash outflows. Debt rose again last year and the dividend looks unaffordable to me – although I suspect it will continue. One to avoid, in my view.

This is a review of the latest results from UK dividend shares that are in my investable universe and may appear in my screening results.

Dividend notes is a new format I'm experimenting with, so any feedback would be particularly welcome - please feel free to comment below or contact me directly.

British Land (BLND)

"we have delivered a good operational performance despite the challenging macroeconomic backdrop"

British Land is one of the UK's biggest listed REITs, with FTSE 100 membership and a market cap of £3.5bn.

Its portfolio is broadly split between prime London office space and major retail parks and multi-use sites, although the company is now diversifying somewhat. You can find full retails of British Land's portfolio here.

These full-year results show a sharp fall in asset values last year, but a more resilient rental performance. While I have some concerns, I can't help but feel the shares probably offer decent value at the current price of c.360p.

Financial highlights: here's a brief summary of some of the main financial metrics from the year ended 31 March 2023.

The company's letting performance appears to have been quite strong:

- Underlying profit up 6.9% to £264m (essentially, this is profit from rental income, excluding the impact of valuation changes)

- Underlying earnings per share up 4.8% to 28.3p

- Dividend per share up 3.3% to 22.64p, maintaining >1.2x cover by underlying earnings

- Estimated Rental Value (ERV) of portfolio up by 2.8%

However, British Land's portfolio of profits suffered a sharp loss of value last year:

- EPRA net tangible asset value down 19.5% to 588p per share

- Statutory net assets down 18.4% to £5,525m

- Statutory loss after tax of £1,039m (FY22: after-tax profit of £965m) – this loss mainly reflects the impact of valuation changes

- Loan-to-value (LTV) ratio up at 36% (FY22: 32.9%)

Higher interest rates mean that property values must fall and/or rental income must rise in order to allow landlords to make a profit. It's not yet clear where this balance will settle, although British Land says it's seeing "early signs of yield compressions for retail parks".

What could go wrong? I can see two main risks for equity holders.

Property values: One is that the value of British Land's properties could continue to fall until its loan-to-value ratio breaches lenders' covenants.

According to the company, the group could withstand a further 36% fall in values across the portfolio "prior to taking any mitigating actions". A further fall on this scale seems unlikely to me, given the quality of the group's properties.

Dividend cut: the other risk is that rental income will not rise quickly enough to cover higher financing costs. This could result in a reduction in the cash profitability of the business and lead to a dividend cut.

There are a lot of moving parts here. But we do know that the British Land has a weighted average interest rate of 3.5% at present, with 97% of debt hedged for the year to 31 March 2024. Beyond this, "76% of projected debt is hedged on average over the next 5 years".

The impact of higher interest rates will hit big corporate borrowers like British Land gradually, as their debt portfolio gradually rolls over.

My feeling from making rough estimates is that the weighted average rate could rise to at least 4.5% without any serious risk to the dividend. I should emphasise this isn't a detailed or reliable calculation, just a guesstimate. But it's one factor informing my view on this stock (and sector) at the moment.

My view: equity investors can buy £1 of British Land assets for 61p at the time of writing. Although I can't rule out the risk that asset vales will fall further, I'm fairly confident that the shares do offer some value at current levels.

I think British Land offers an opportunity for investors to benefit from a revaluation closer to NAV over the next few years. In my view, the 6% yield looks reasonably safe too, although I would probably price a small cut into any models to be prudent.

On balance, I see British Land as a buy for value at current levels.

Experian (EXPN)

"We delivered very strong results in FY23, reflecting a combination of new business wins, new products and expansion into higher growth markets"

Experian is known as a credit reference agency in the UK, but prefers to style itself as "the global information services company".

This is a business I view as a high-quality compounder, but I've always struggled with the valuation. These results don't do much to change that view.

Last year saw revenue rise by 5% to $6,619m, while pre-tax profit fell by 19% to $1,174m. My calculation suggests free cash flow excluding acquisitions fell to $960m last year (FY22: $1,324m), so there's good alignment with profit.

Management prefer a more heavily adjusted 'benchmark EBIT' figure, which last year excluded more than $500m of (mostly) non-cash charges. However, given the free cash flow alignment, I prefer to rely on statutory profits.

Trading appears to have been fairly strong, with organic revenue growth of 7% on a constant currency basis.

Revenue from business customers rose by 6%, while consumer revenue was 11% higher. Experian says it how has 168 million free consumer members globally.

I'm not sure how many paid consumer customers there are, although of course I imagine the data provided by free customers probably feeds into services that are sold to business customers.

Experian's profitability remains strong, although down slightly from last year. The company reports a Benchmark EBIT margin of 27.4% and ROCE of 16.5%.

My sums, based on statutory profits, give an operating margin of 19.1% and ROCE of 14.5%.

Net debt of $4bn equates to 1.8x EBITDA or four times free cash flow. I don't see much to worry about, given the profitability and cash generation of the business.

Outlook: the company expects to see organic revenue growth of 4-6% during the coming year, with "modest margin improvement".

Broker forecasts ahead of the results suggested adjusted earnings of $1.46 per share, putting the stock on a forecast P/E of 23 with a 1.9% dividend yield.

My view: I haven't been through Experian's results in any detail, because it's not really priced at a level where I'd consider investing.

My calculations suggest Experian is trading on a FCF/EV yield of 2.9%, with an EBIT/EV yield of 3.6%. While this might not be an outrageous valuation for a high-quality business, it's not cheap enough for me.

However, my view of this business as a buy-and-hold investment remains positive. If the dividend yield rose to somewhere above 2%, I might consider buying.

BT Group (BT-A)

"We have delivered our outlook for FY23"

In these dividend notes I'm trying to focus on companies I have at least some interest in owning. But I couldn't resist the lure of looking at BT's latest results.

The telecom group's latest numbers triggered a 5% slump in the firm's already battered share price. It's not hard to see why.

Financial highlights: BT's revenue fell by 1% to £20,681m last year, while the group's pre-tax profit dropped 12% to £1,729m. By my reckoning, revenue has now fallen every year since 2017.

BT's net financial debt rose by £1.3bn to £13.5bn, for reasons I'll explain shortly.

The operating margin of 12.7% and return on capital employed of 6.3% were almost unchanged from last year. While the operating margin looks reasonable, I would guess that ROCE of 6% is barely enough to cover the group's cost of capital. In other words, BT may be running to stand still.

One bright spot was that net cash inflow from operating activities rose by 14% to £6,724m. However, most of this was swallowed up by capital expenditure of £5,056m. Excluding spectrum, this figure was 5% higher than last year.

The dividend was held unchanged at 7.7p, giving a 5.5% yield.

Operating highlights: chief executive Philip Jansen says that "Openreach is competing strongly and it's clear that customers love full fibre". They probably do.

But while customers are signing up for full fibre services, they're also abandoning their legacy copper lines. Meanwhile, competition from altnet fibre networks is increasing. As a result, BT's pricing power does not seem to be improving – hence another year of falling revenues.

Free cash flow & dividend: BT's normalised (adjusted) measure of free cash flow fell by 5% to £1,328m last year. This was at the lower end of the company's guidance, but even so, I don't think it tells the full story.

Looking through the cash flow statement, my sums suggest that BT suffered a free cash outflow of c.£290m last year, before payment of the £751m dividend.

In other words, a cash outflow of c.£1,040m in total. This also aligns with the £1.2bn increase in net financial debt last year.

The outflow was driven by the £994m pension deficit contribution and the additional £700m of capex last year. But we could also argue that the outflow was also driven by a dividend that remains unaffordable, given the company's spending commitments.

Paying dividends out of borrowed money makes no sense to me, given the other priority demands on the company's cash flows. But I'd imagine the payout might continue for a while yet, to prevent ructions amongst the group's shareholders and any further share price collapse.

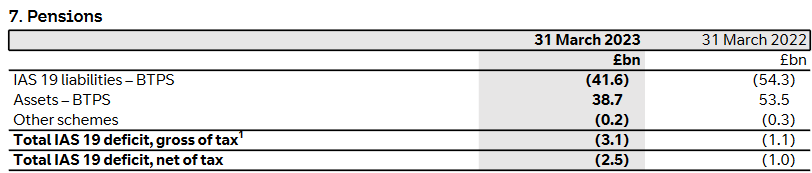

Pension: BT's pension deficit rose by £2bn to £3.1bn last year, despite the company paying £1bn into the scheme. The company says that the increase in the deficit was linked to "negative asset returns mainly due to higher real gilt yields".

However, I think there's a second factor we need to consider. Borrowing the method used by my friend and podcast partner Maynard Paton, I looked up the annual benefits paid by BT's pension scheme.

We don't have this year's annual report yet, but in FY21 and FY22, annual benefits paid totalled about £2.8bn.

Today's results show that BT's pension scheme assets were valued at £38.7bn at the end of March 2023.

Paying out £2.8bn sustainably from £38.7bn of assets would require a 7.2% return. That seems unlikely to be achievable with typical pension scheme assets such as government bonds.

For this reason, I suspect BT's pension scheme is likely to remain a cash black hole. Forecasts in last year's annual report show cash contributions of at least £600m per year until 2030, with a provision for additional contributions if needed.

My view: BT looks uninvestable to me. I don't think there's much likelihood that the company will create any value for shareholders for the foreseeable future.

For investors wanting a reliable 5.5% dividend yield, I think there are many better choices elsewhere.

Disclaimer: This is a personal blog/newsletter and I am not a financial adviser. The information provided is for information and interest. Nothing I say should be construed as investing advice or recommendations. The investing approach I discuss relates to the system I use to manage my personal portfolio. It is not intended to be suitable for anyone else.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.