The Dividend Note - 30+ years of dividend growth - CRDA, BNZL, SXS, MACF (01/03/24)

I review the latest results from Croda International, Bunzl and Spectris, all of which have delivered 30+ years of dividend growth. Plus small-cap packaging specialist Macfarlane.

Welcome back to The Dividend Note. This is a weekly review of results from dividend stocks that look potentially interesting to me.

The companies covered this week could all loosely be described as industrials. Three out of four of them boast dividend growth records of at least 30 years or more.

The fourth company, small-cap Macfarlane, could be well on the way to building such a record, in my opinion.

Many UK manufacturing and industrial stocks have suffered from customer destocking, supply chain disruption and cost inflation over the last couple of years.

However, the best operators are still delivering fairly stable results and continue to offer long-term growth potential. I reckon all four of these companies could fall into this category – they are all on my watch list as possible future portfolio purchases.

Companies covered:

These notes contain a review of my thoughts on recent results from UK dividend shares in my investable universe. In general, these are dividend shares that may appear in my screening results at some point.

Please note that my comments reflect my personal views and are not investment advice or recommendations. Please do your own research and seek professional advice if needed. Full disclaimer here.

- Croda International (LON:CRDA) - 2023 results were poor, as expected, but this chemicals group looks in reasonable health and positioned for a return to growth. The valuation looks a little full to me, but Croda stays on my watch list.

- Macfarlane (LON:MACF) - a solid set of results from this small-cap packaging group, despite more difficult market conditions in 2023. The shares aren't quite as cheap as they were, but I remain a fan.

- Bunzl (LON:BNZL) - solid results in a challenging year. This distribution business is a classy operator, in my view. I explain how the business has consistently created value for shareholders over many years.

- Spectris (LON:SXS) - solid results from this precision measurement specialist for 2023, against a more difficult backdrop. But the outlook for 2024 seems a little more subdued. I like the business but continue to hope for a better buying opportunity.

Croda International (CRDA)

"1p increase in full year dividend with 32 years of unbroken dividend progression"

2023 full-year results / Mkt Cap: £6.4bn

FY24 forecast dividend yield: 2.4%

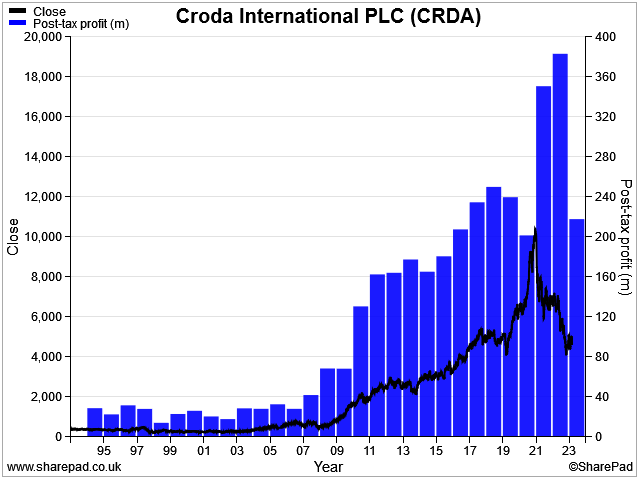

Long-term shareholders in chemicals group Croda International have seen their shares halve since hitting an all time record of more than £100 in late 2021.

Two years of record profits during the pandemic were driven by a contract to supply "lipid-based drug delivery technologies" used in the Pfizer-BioNTech Covid-19 vaccine.

This tailwind has now dropped out of the numbers, as expected. But the impact of this profit reset was made worse by customer destocking last year, prompting Croda to cut its profit guidance in June.

The chart tells an interesting picture, showing both profits and the share price back at pre-pandemic levels:

I'm interested to see if this could be a good time for me to consider buying the shares for my dividend portfolio.

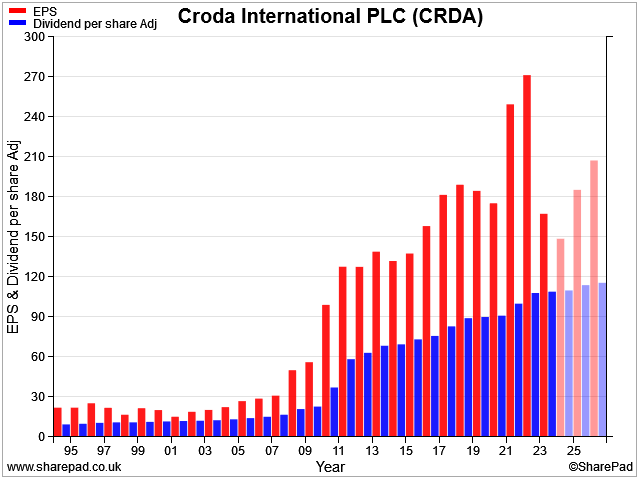

After all, Croda was founded in 1925 and has increased its dividend every year for the last 32 years. If the business can now pick up where it left off prior to the pandemic, I reckon now might be an interesting time to buy.

Let's take a look at the numbers to find out more.

Results summary: Croda's headline numbers for 2023 do not make for pleasant reading:

- Revenue fell by 19% to £1,694.5m

- Operating profit fell by 44% to £247.5m

- Operating margin fell to 14.6% (2022: 21.2%)

- Adjusted free cash flow rose by 5.1% to £165.5m

- Net debt increased by 82% to £537.6m due to an acquisition in July 2023

- Dividend up 0.9% to 109p per share

Some of these figures were influenced by the divestment of the PTIC business in 2022. But even allowing for this, the trend was not Croda's friend last year.

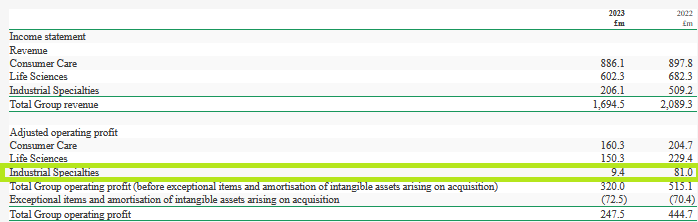

Croda reports three operating segments, Consumer Care (beauty/personal care), Life Sciences (pharma/agriculture) and Industrial Specialities (coatings/additives).

This segmental breakdown shows a decline in all three, but the industrial business was particularly hard hit, with adjusted profits down 88% to just £9.4m:

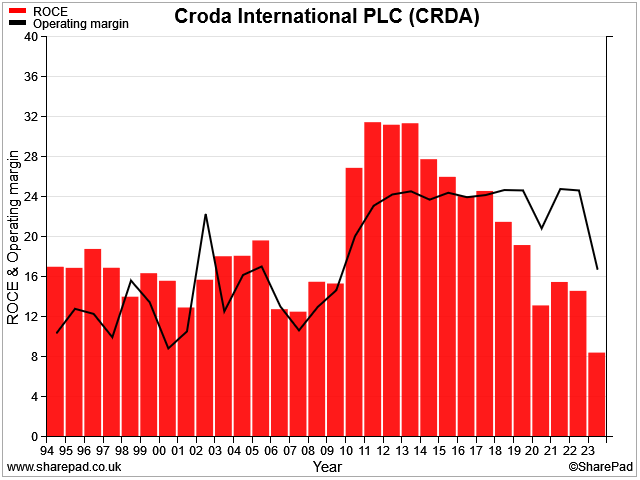

Profitability: operating margins fell sharply last year and I estimate the group generates a return on capital employed of around 8%.

According to SharePad data that's the worst ROCE result for 30 years:

Free cash flow: the company's adjusted measure of free cash flow improved by 5% to £165.5m last year. This represents excellent cash conversion from 2023 net profit of £172.1m.

Checking the free cash flow statement, my sums give a slightly more conservative figure of c.£125m, albeit still excluding acquisition activity.

Even using the company's own measure, my sums suggest the shares are trading with a free cash flow yield of just 2.6%. That's enough to cover the 2.4% dividend yield, but doesn't seem compellingly cheap.

Outlook: much will depend from here on whether Croda can return to the double-digit profitability and steady growth shareholders have enjoyed in the past:

The company's guidance suggests 2024 may be difficult, but is more bullish on a return to significant growth in 2025.

This seems to be partly a verdict on macro conditions, but also a reflection on new products that are expected to enter the market from 2025 (my bold):

"With our strong balance sheet, improving cash flow and consistent investment in our refocused portfolio, Croda is well positioned to take advantage of the demand recovery when it occurs. We expect the Group's performance to accelerate from 2025, generating continued increasing returns for our shareholders."

Broker forecasts suggest earnings of 151p per share in 2024, rising by 22% to 185p per share in 2025. Those numbers put the stock on a 2024 P/E of 30, falling to a P/E of 25 in 2025.

My view

I have some respect for Croda's near-100 year history and 32-year track record of dividend growth.

The balance sheet looks fine to me and the business model appears to be focused on areas where I would expect growth to continue over the coming years.

On a long-term view, I think Croda shares could prove to be reasonably priced if the business can deliver the kind of growth its achieved in the past.

However, an EBIT yield of 3.5% and sub-3% free cash flow yield do not leave much room for disappointment. For now, I'm staying on the sidelines, but Croda is a stock I will continue to watch and would consider owning.

Macfarlane (MACF)

"Group profit before tax ahead of previous year"

2023 full-year results / Mkt cap: £195m

FY24 forecast yield: 3.1%

I covered this small-cap packaging group in an in-depth review in November 2023 and was broadly impressed. While I noted some risks, I did not see too much to be concerned about.

This week's half-year results don't alter that view. The group's bolt-on acquisition strategy continued to tick over last year and its high-margin manufacturing division helped to offset some weakness in the distribution business.

Results summary: Macfarlane managed to eke out an increase in pre-tax profit last year, a drop in sales and a higher corporate tax rate hitting earnings:

- Revenue down 3% to £280.7m

- Operating profit up 3% to £22.1m

- Operating margin: 7.9% (2022: 7.4%)

- Earnings per share down 5% to 9.44p

- Dividend up 5% to 3.59p per share

Free cash generation for the year benefited from some favourable moves in working capital. Impressively, I think, the business ended the year with net cash at bank of £0.5m, despite £16.6m of acquisition and capex spend last year.

Divisional highlights: Macfarlane's business is divided into two segments for reporting:

- Packaging Distribution: sales fell by 6% to £244.9m last year, while operating profit fell 3% to £16.5m, giving an operating margin of 6.7%. "Good sales momentum in Europe" helped to offset "weak demand" from customers in the UK and Ireland. Recent acquisitions PackMann and Gottlieb are said to be performing well.

- Manufacturing operations: this is a niche business manufacturing packaging for higher value industrial applications. Sales rose by 16% to £35.8m in 2023, while operating profit rose by 26% to £5.6m. This implies a margin of 15.6% and highlights the value of this business, despite its relatively small scale.

Profitability: my sums suggest Macfarlane generated an overall return on capital employed of 14.8% last year, which is consistent with the average performance over the last five years.

Outlook: management expect the year to be challenging due to uncertainty over customer demand. But the board is confident of continued progress in 2024 with the benefit of new business momentum, further acquisitions and "effective management".

House broker Shore Capital has left 2024 estimates unchanged at 12.4p per share, pricing the stock on a forecast P/E of 10.

My view

On the basis that 2023 is likely to be a low point for volumes, I think Macfarlane continues to look reasonably priced at current levels.

My sums give a trailing EBIT yield of 9.4%, supported by good cash conversion. A forecast dividend yield of 3.1% is fairly average but looks well supported to me.

If the dividend growth rate of 5% per year is maintained in line with forecasts, then the current share price implies an expected return (dividend yield plus growth) of just over 8% this year.

Macfarlane may not be obviously cheap in the way I thought it was in November, but I would still be comfortable buying the shares at current levels.

Bunzl (BNZL)

"31st consecutive year of annual dividend growth; total dividend per share growth of 8.9%"

2023 full-year results / Mkt cap: £10.6bn

FY24 forecast dividend yield: 2.3%

Back in August last year, I wrote about Bunzl's half-year results and said I thought shares in this distribution specialist looked fairly priced.

Fast-forward six months and Bunzl's share price has risen by a further 10% or so, even though profit guidance during this period remained pretty much unchanged.

For the uninitiated, Bunzl is a distribution group that supplies a huge range of goods-not-for-resale and consumables to business customers all over the world. Examples include catering consumables, cleaning supplies, healthcare equipment, safety gear and much, much more.

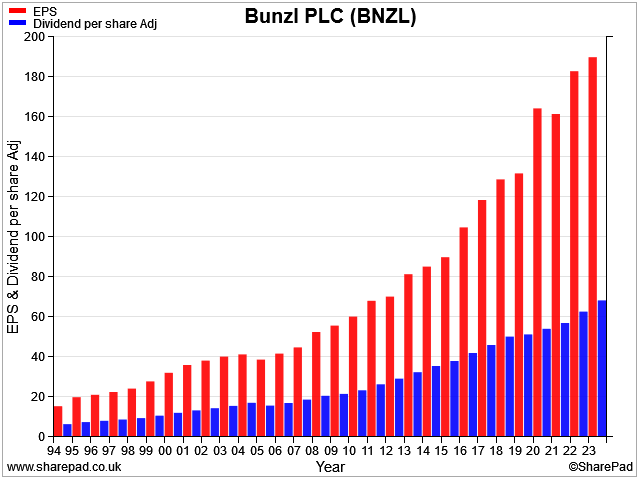

A consistent strategy built around organic growth and bolt-on acquisitions has delivered an enviably long run of dividend and earnings growth:

Bunzl is the kind of stock I would be interested in owning in my dividend portfolio at the right price, so I like to keep an eye on its trading performance.

Results summary: 2023 saw a rare fall in revenue, but a recovery in margins meant that there was still an improvement at the bottom line.

- Revenue down 2% to £11,797.1m

- Operating profit up 12.5% to £789.1m

- Operating margin: 6.7% (2022: 5.8%)

- Pre-tax profit up 10.1% to £698.6m

- Basic earnings per share up 10.9% to 157.1p

- Dividend up 8.9% to 68.3p per share

Bunzl's statutory profits were boosted by gains from the disposal of its UK healthcare business last year, but I've used them anyway as I feel the company's adjusted profits exclude too many items that I would prefer to include.

For comparison, last year's adjusted earnings per share were 191.1p, 21% above its basic earnings per share.

Free cash flow: I like to include amortisation charges in the measure of profit I use to calculate return on capital employed. This is because amortisation often reflects past capital expenditure decisions – real cash outflows. This is especially true with an acquisitive business such as Bunzl.

However, the counter-argument for excluding amortisation is that it does not reflect the cash generated by the ongoing business, once acquired. This certainly seems to be true here.

Bunzl's cash conversion is generally excellent and results for both 2022 and 2023 show free cash flow that is much closer to adjusted profit than it is to statutory profits:

| Metric/Year | 2023 | 2022 |

| Free cash flow* | £628m | £598.9m |

| Adjusted net profit | £640.3m | £616.8m |

| Reported net profit | £526.2m | £474.4m |

*my calculation

My 2023 free cash flow estimate of £628m gives Bunzl a free cash flow yield of 5.1% – not necessarily too expensive, in my view.

Profitability: profit margins are always fairly low in distribution businesses. But decent returns on capital employed are possible through efficient use of working capital, good scale, and skilled management.

Bunzl has these qualities, in my view, and has consistently generated ROCE of around 14% in recent years. Modest use of debt means that returns on equity are around 20%.

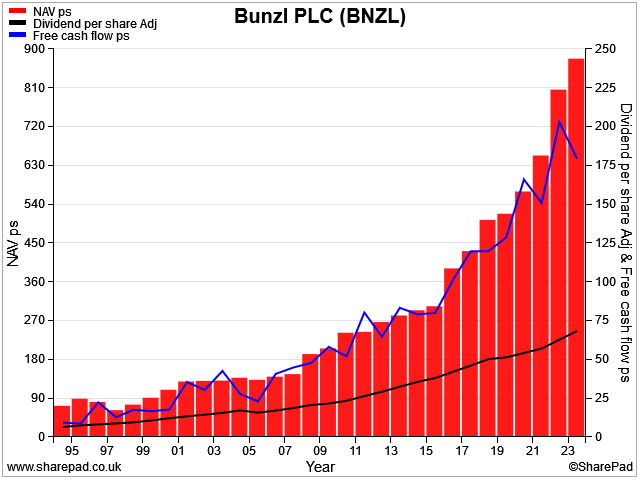

This wonderful chart shows how Bunzl has created lasting shareholder value over the last 30 years by compounding reinvested capital to drive sustainable growth in free cash flow and dividends:

Outlook: there was no new outlook statement for 2024 in these results. Instead, the company simply reiterated the 2024 profit guidance provided with its pre-close statement in December.

"the Group expects some revenue growth in 2024, at constant exchange rates, driven by announced acquisitions and slightly positive organic growth. Group operating margin is expected to be broadly in-line with 2023, and to remain substantially higher compared to pre-pandemic levels, driven by the higher margin acquisitions acquired since then, as well as an underlying margin increase"

Broker consensus forecasts suggest adjusted earnings of 185p per share for 2024, which would represent a slight drop from last year's adjusted figure of 191p.

However, a forward P/E of 17 is slightly below the level the stock has traded at in recent years and does not look entirely unreasonable to me.

My view

My number crunching suggests Bunzl is trading with an EBIT/EV yield of 6.4% and a free cash flow yield in excess of 5%.

Given the strength of the Bunzl's track record, I am tempted to believe that this could be a reasonable entry point for my portfolio. Bunzl is another stock that remains on my watch list.

Spectris (SXS)

"Dividend per share increase of 5%; 34 years of continuous dividend growth"

I'll wrap up with a quick look at the 2023 results from Spectris. This FTSE 250 group a precision measurement specialist. It provides software, high-tech instruments, and test equipment for industrial clients, who benefit from the insight and analysis Spectris products provide.

34 years of continuous dividend growth is an impressive record, I think. These 2023 numbers display the kind of consistency that's needed to produce such a strong result.

As I've pointed out before, Spectris does make somewhat generous use of adjusted profits. I have reported the main statutory figures here, which I generally prefer to use:

- Revenue up 9% to £1,449.2m

- Operating profit up 9% to £188.6m

- Operating margin flat at 13.0%

- Earnings per share up 31% to 140.3p

- Dividend per share up 5% to 79.2p

- Net cash of £138m (2022: £228m)

Trading commentary: CEO Andrew Heath says like-for-like sales rose by 10%, while adjusted operating profit was 18% higher on a LFL basis.

At a divisional level, both sales and adjusted margins improved:

- Scientific: LFL sales up 12%, adj operating margin up 0.7% to 22%

- Dynamics: LFL sales up 6%, adj operating margin up 2.2% to 17.2%

Looking across different customer sectors, LFL growth was positive across the board except for life sciences/pharmaceutical. The company says this reflects normalisation of demand after strong growth during 2021 and 2022:

Cash flow/debt/buybacks: underlying free cash flow in 2023 benefited from a normalisation of working capital, after extra outflows in 2022 to support higher stock levels and extended receivables.

Even so, the business ended the year with a reduced net cash position of £138m (2022: £228m). This seems to be due to the £115m spent on share buybacks during the year.

It's a reasonable choice to buyback shares with genuine surplus cash, but personally I'd prefer a special dividend – existing shareholders get no tangible benefit from buybacks unless they sell.

Outlook: CEO Heath sounds positive about the year ahead, but with a caveat (my bold):

"We expect to deliver another year of further progress in 2024, including margin expansion, after taking into account the impact of the Red Lion disposal"

This $345m disposal was agreed in December and is expected to complete shortly. Red Lion generated £21.9m of adjusted operating profit in 2023, around 8.3% of the total (this was reported in the "other" segment in the table above").

The loss of Red Lion means that overall results are expected to be a little flatter than Heath's bullish comment might suggest.

Broker consensus forecasts have been trimmed following these results and suggest adjusted earnings could rise by just 1.2% to 202p per share in 2024.

Dividend growth is expected to be stronger, with an expected payout of 85p, up 7%.

Those numbers price the stock on 17 times earnings with a 2.4% dividend yield – not necessarily too expensive for this business, in my view.

My view

I prefer to use EBIT yield (EBIT/EV) rather than P/E as a measure of valuation. Crunching the numnbers gives an EBIT yield of 5.5% for Spectris, based on last year's reported operating profit.

That's a little lower than I would like to pay, but I don't think it's really expensive.

If Spectris shares were to drift closer to £30 this year – or even below – without a significant change to expectations, I might be tempted to buy some.

Roland Head

Disclaimer

This is a personal blog/newsletter and I am not a financial adviser. All content is provided for information and educational purposes only. Nothing I say should be interpreted as investing advice or recommendations.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.