Is dividend share RWS Holdings an AI bargain?

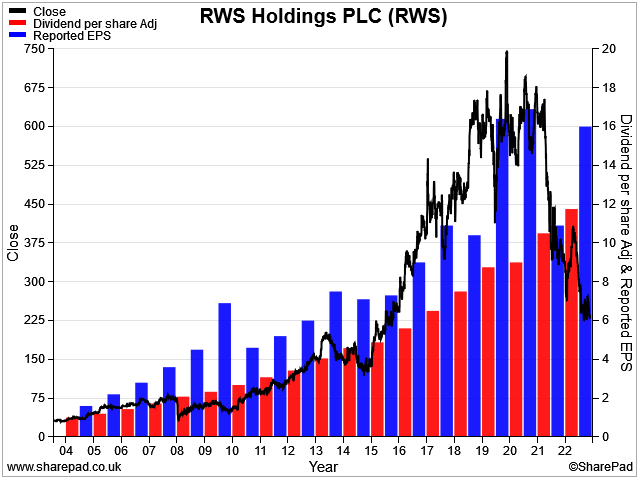

Shares in AIM-listed RWS Holdings (LON:RWS) have fallen by nearly 70% from their pandemic peak and now yield over 5%.

Shares in translation and structured content specialist RWS Holdings (LON:RWS) are trading at levels last seen in 2016.

I'd have expected some kind of post-pandemic slump, given the Covid-era hype over all things tech and AI-related.

But RWS's earnings per share and its dividend have both doubled since 2016. Has the sell-off created a buying opportunity?

RWS generated about £750m of revenue last year and has a £900m market cap. But its shares currently trade on a forecast price/earnings ratio of just nine, with a tempting 5% dividend yield.

I'm looking for a new stock for my dividend portfolio to replace healthcare software group EMIS, where a takeover bid is finally going through after some delays.

I've been taking a closer look at RWS and running the shares through my scoring system to see if this firm could be a suitable choice for my portfolio. Here's what I've found.

Table of contents

- History - 20 years of growth

- Will AI make RWS redundant?

- Crunching the numbers - how does RWS score in my screening system?

- Dividend culture - 19 years of unbroken growth

- Dividend safety - very strong

- Dividend growth - well supported

- Dividend yield - RWS's yield is at a post-2008 high...

- Valuation - I think the shares could be very cheap

- Profitability - a downward trend disappoints

- Fundamental health - a clean sheet

- Conclusions - is RWS a contender to fill the upcoming vacancy in my portfolio?

RWS: 20 years of growth

RWS provides language, content management and intellectual property (IP) services to a wide range of corporate and public sector customers.

The company currently has around 7,700 staff in 36 countries, supported by a network of 29,000 freelancers (mainly translators) in 169 countries. RWS says it can support 270 language pairs and has substantial in-house technology assets, including AI services.

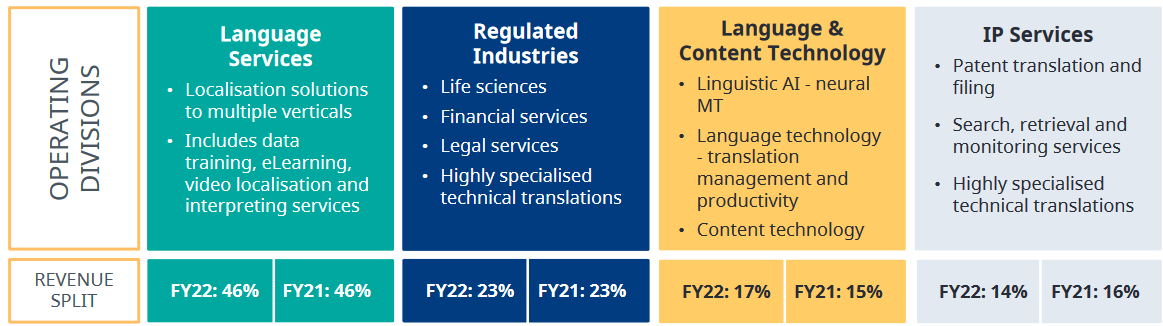

The business is structured into four operating divisions. These cover a wide range of services – from fairly general commercial translation, to complex and specialised intellecutal property services:

History: Executive chairman Andrew Brode acquired RWS from private equity group 3i in 1995. Brode then listed the business on the AIM market in 2003.

He remains the group's largest shareholder, with a 23% position worth over £200m. This suggests to me that RWS is still very much an owner-managed business.

Brode has previously led a series of companies that have subsequently been sold. He's currently also the largest shareholder and non-executive chairman of £600m AIM group Learning Technologies.

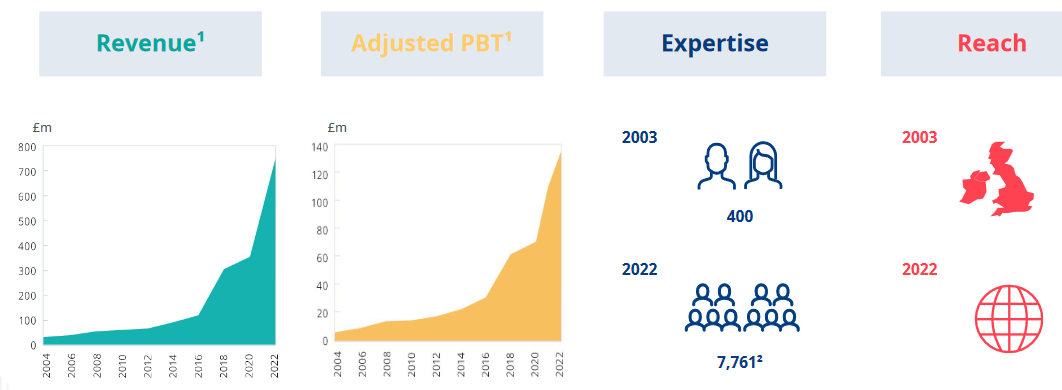

RWS has expanded considerably over the last 20 years:

Some of this growth has been driven by acquisitions, notably big deals in 2017 and 2020. These correspond to the big shifts in profit shown in the chart above:

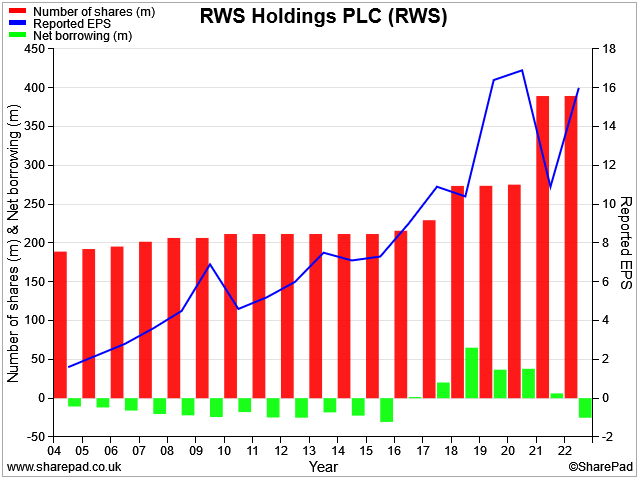

Funding these deals has required a certain amount of debt, but this has been repaid promptly and RWS has generally maintained a net cash balance.

In the meantime, earnings per share have trended steadily higher, suggesting to me that shareholders have not suffered too much from this dilution:

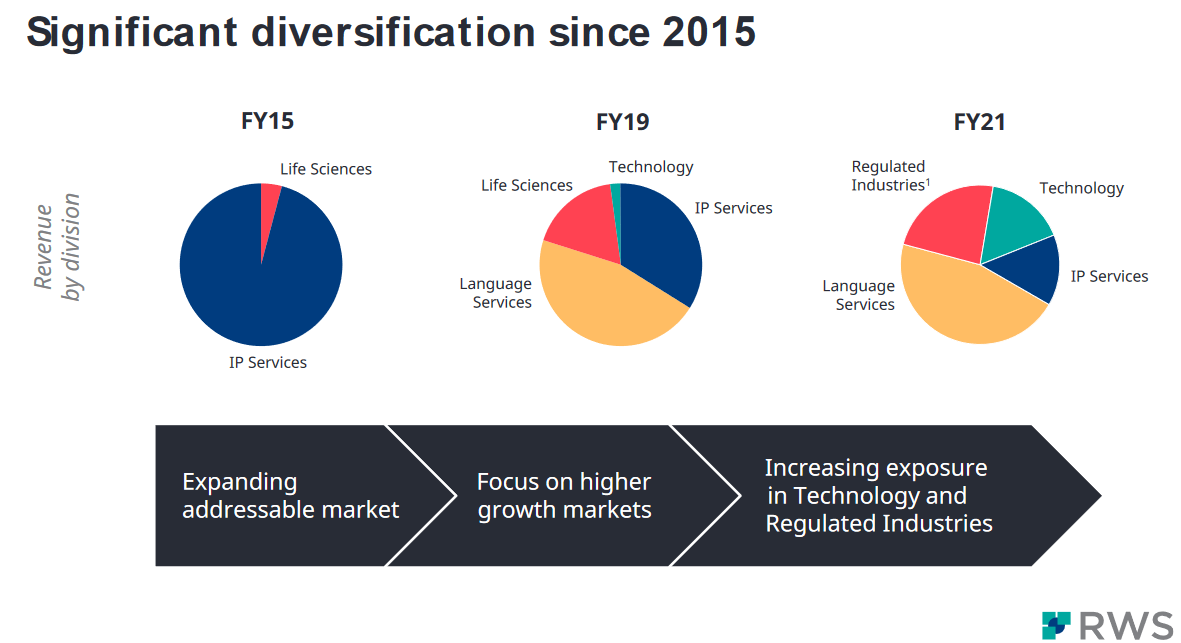

This acquisitive growth has supported a substantial degree of diversification since 2015:

RWS's now appears to enjoy strong positions in a number of key markets, based on this summary of the group's customer base:

The company says that its top 30 customers have an average tenure of 15 years and generated 43% of group revenue in 2022. That sounds like a fairly solid foundation to me.

Current trading: market conditions do not seem entirely favourable for RWS at the moment.

In its half-year presentation to analysts, RWS said it was facing a combination of macroeconomic headwinds and regulatory bottlenecks. These had lead to a slowdown in new client decision making, lower levels of activity, and greater client focus on costs.

In response, RWS is planning cost savings of £10m this year and £25m next year. The company is also continuing to focus on sales efforts on higher-value IP markets and developing new services, including offering its own AI-centred products to customers.

Half-year results: I covered RWS's recent half-year results here. But in summary, revenue rose by just 2.5% to £366.3m, while earnings per share fell 11% to 5.4p for the six-month period.

On an organic constant-currency basis (i.e. excluding acquisitions and exchange rate movements), revenue fell by 7% during the first half, suggesting a slowdown in translation volumes.

Cash generation remained excellent, with free cash flow of £30m from net profit of £21m. But a combination of acquisitions, capex, and dividend payments meant that net cash fell from £72m to £58m between 30 September and 31 March (RWS has a 30 Sept year end).

Outlook: full-year guidance was left unchanged at the half-year, with management continuing to expect a second-half weighting to profits as various bottlenecks ease.

SharePad forecasts suggest earnings of 24.4p per share, with a dividend of 12.2p. That prices the shares on 9.6 times forecast earnings, with a prospective dividend yield of 5.2%.

I'm pretty confident that if the future was like the past, I could rely on RWS returning to growth as economic conditions ease. The elephant in the room, of course, is AI. The future isn't going to be like the past.

Will AI make RWS redundant?

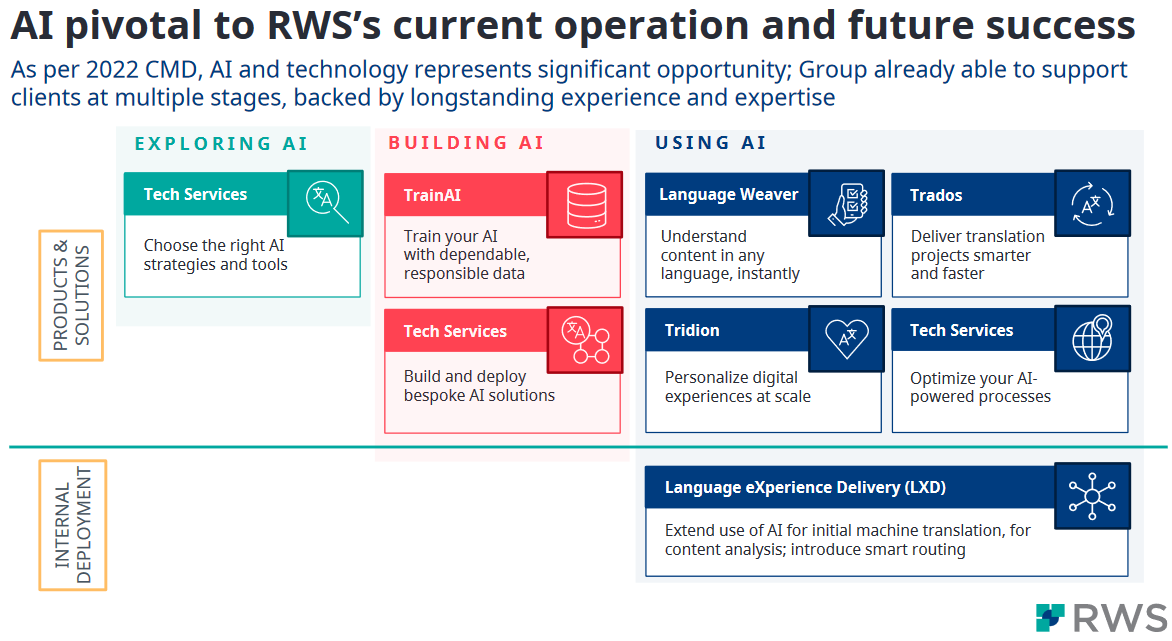

RWS says that AI and technology "represent significant opportunity" (my bold throughout):

"RWS has longstanding AI capability and expertise in relation to localisation, language and content technology and content development, with a pioneering machine translation solution (Language Weaver), a full data services proposition (TrainAI) and deployment of AI-functionality in our Tridion and Trados products, all of which make us a significant beneficiary of developments in AI."

According to the recent half-year results, the majority of its translation work already flows through an AI-supported process:

"With 60% of the words that we translate through the LXD being supported by AI, we are already extensive users, benefiting from the efficiency opportunities this technology brings in the medium term"

I think the idea is that RWS uses AI in-house where it can achieve cost or speed savings, while overlaying human expertise to ensure a higher standard of quality and reliability.

At the same time, the company is hoping to sell its curated data models and AI services to clients:

My feeling is that the wide availability of cheap general AI services will inevitably cause some attrition at the lower-value end of RWS's solutions spectrum.

On the other hand, I expect that many of RWS's core markets will continue to require a standard of quality and specialism that won't be freely available.

From what I understand, many of RWS's translations need to be guaranteed to be correct in legal, scientific, and regulatory terms. Presumably the company's service offering includes some liability for errors, much like an accountant or lawyer might offer.

Ultimately, you can't fine software or send it to prison. Only people and corporations can accept liability for errors. I don't see many generalist or low-cost AI translation service providers offering this kind of accountability and service guarantee in the near future.

After all, the leading mainstream AI services are currently known to suffer from hallucinations – they invent facts that sound plausible.

I could be wrong: I fully accept that I could be completely wrong about all this. AI is certainly going to change the world, we just don't yet know how. New services could improve quickly and become available at prices that will leave RWS looking bloated and redundant.

I certainly see AI as a risk as well as an opportunity for RWS, regardless of what the company's management is saying.

Investors need to do their own research and form their own view on this. My comments above represent my working hypothesis at the moment. But this view may change (and may be wrong!).

However, my approach to investing is not just about a company's story. As a systematic investor, I place a heavy weighting on historic financial performance. Let's move on and see how RWS stacks up in this regard.

RWS Holdings: crunching the numbers

Description: a specialist in high-quality translation, content management, and intellectural property services, such as patent translation.

| RWS Holdings (LON: RWS) |

Quality Dividend score: 72/100 | Forecast yield: 5.2% |

| Share price: 233p | Market cap: £899m | All data at 24 August 2023 |

Latest accounts: half-year results for the six months to 31 March 2023

In the remainder of this review, I'll step through the different stages in my dividend screening system and explain whether I think RWS could be a suitable addition to my quality dividend portfolio .

Unless specified otherwise, the financial data I use in this process is drawn from SharePad.

Dividend culture: excellent

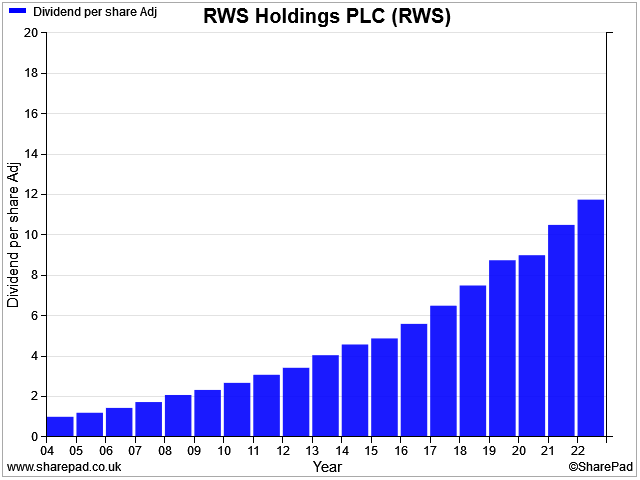

RWS Holdings listed on AIM in late 2003 and has increased its dividend in each of the 19 years since then.

That's not quite long enough to earn a top score in my screening system, but it's a very impressive result nevertheless.

I estimate that 23% shareholder Andrew Brode received nearly £11m in dividends last year. With him in the chairman's seat, I'm confident that RWS has a strong dividend culture.

RWS scores 3/5 for dividend culture in my screening system.

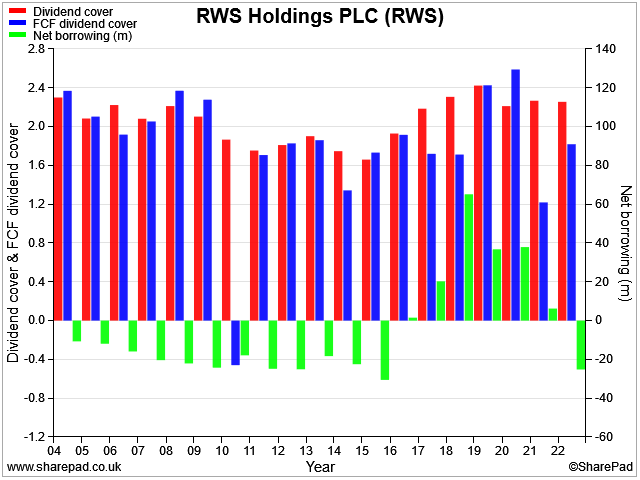

Dividend safety: very strong

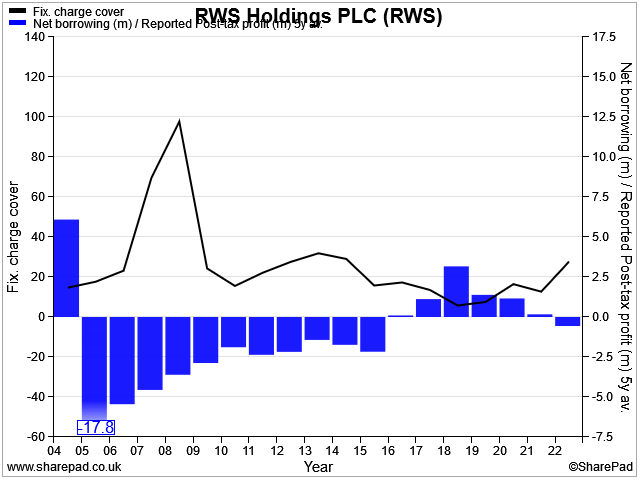

I score shares for dividend safety by looking at the level of earnings and free cash flow cover for the dividend.

My score also includes a measure of leverage, which I've represented here as net borrowing in order to simplify the graph:

I can't see anything to dislike here. RWS's dividend has been covered comfortably by earnings in each of the last 19 years. Free cash flow cover has only fallen below 1.2x on one occasion during that period.

As we've seen already, the company has generally maintained a net cash position, except during a period when several major acquisitions were made.

Past performance is no guide to future returns. But historically, I think RWS's dividend has looked very safe.

RWS scores 4/5 for dividend safety in my screening system.

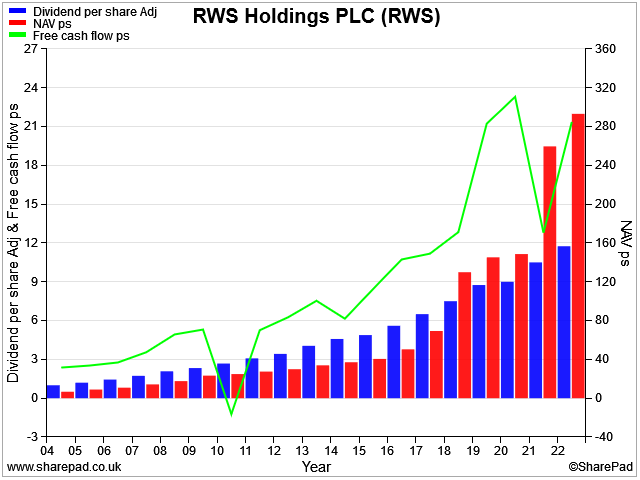

Dividend growth: well supported

When rating a company's dividend growth record, I do look at the rate of growth. However, my main goal is to try and gauge how sustainable this growth has been.

In other words, has dividend growth been well supported by free cash flow and net asset value per share growth? Poorly supported dividends are far more likely to be cut, in my experience.

This chart compares these three metrics for RWS. We can see that both free cash flow and NAVps have trended steadily higher. This suggests to me that the dividend-paying capacity of the business has increased in step with the growth of the dividend.

RWS scores 4/5 for dividend growth in my screening system.

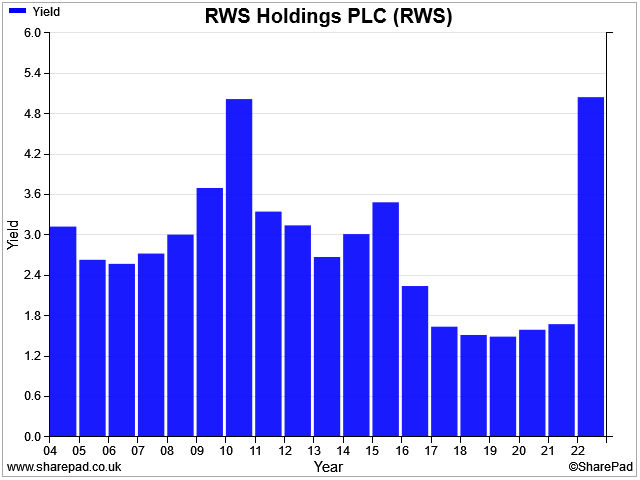

Dividend yield: post-2008 high

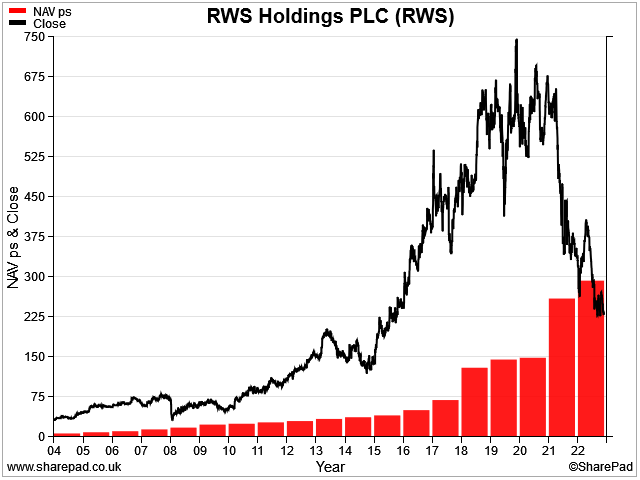

RWS has not generally been a high-yield stock. But the share price slump suffered by RWS over the last two years has caused the stock's trailing dividend yield to rise to the highest level since 2010:

I've seen this with a number of stocks recently, including some I've written about here. I have to ask whether this is a sign of problems ahead, or whether these shares have been oversold and now offer contrarian value.

Unfortunately, the answer to this question is usually only obvious with hindsight.

In the meantime, my scoring system tells me that on a medium-term view, RWS has typically been a stock with a fairly average yield.

RWS scores 2.7/5 for dividend yield in my screening system.

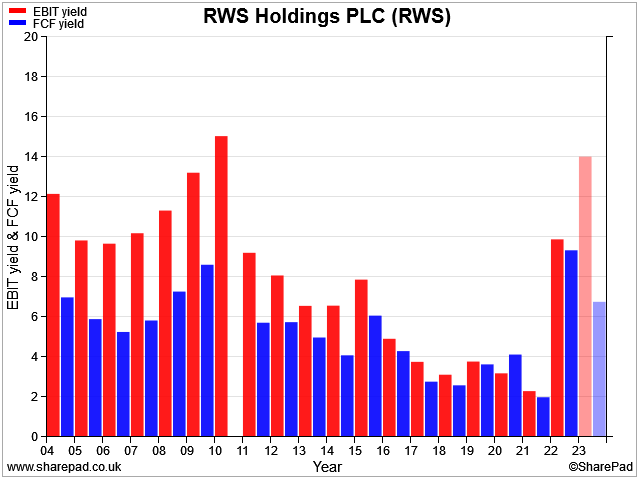

Valuation: cheap?

The share's unusually high dividend yield (above) suggests to me that RWS shares could be cheap at the moment.

I think the stock's valuation supports this view, but it also offers another possible interpretation – perhaps RWS shares had become too expensive.

This chart shows the stock's historic EBIT (EBIT/EV) and free cash flow yields. These are the main valuation measures I use in my screening system.

We can see that the stock's EBIT and FCF yields ranged from 2%-4% between 2017 and 2021. That seems quite a full valuation to me.

In particular, I would argue that the 2% EBIT/FCF yields on offer in 2021 were decidedly unattractive. The shares have since fallen by 50%, despite profits rising sharply in 2022.

I've already talked about some of the risks facing the business. But I'd like to highlight two important positives that I take from this chart:

- Free cash conversion from operating profit appears to be excellent, especially since 2015 (the red and blue bars are almost the same height each year)

- Based on last year's results, the shares look very attractively valued, with a trailing free cash flow yield of over 9%

- Broker forecasts (shaded lines) suggest operating profit will rise this year but free cash flow will fall. In either case, the prospective yields implied still seem attractive to me.

£50m share buyback: one other point of interest regarding the valuation is that RWS launched a £50m share buyback programme alongside its half-year results. This is equivalent to just over 5% of the current market cap – a big buyback.

The company says it has enough headroom under its current banking facilities (and cash pile) to fund the buyback while maintaining the dividend and pursuing further acquisitions.

I'm only speculating, but RWS shares are currently trading below book value for the first time in their history, as far as I can tell:

The group's assets are dominated by goodwill and intangibles from acquisitions. But if these deals were fairly valued and the acquired assets perform as expected, then I reckon this buyback could prove to be good value for shareholders.

On the other hand, in a worst-case scenario, this big buyback could simply prove to be an expensive effort to prop up flagging earnings.

Given that Andrew Brode has run the business since 1995 and holds 23% of the shares, I'd hope that his superior insight will produce a positive result. But it seems a pretty confident move at present, all the same.

On balance, I have to conclude that RWS shares look very cheap at the moment, unless the business is about to suffer serious new problems.

RWS scores 4/5 for valuation in my screening system.

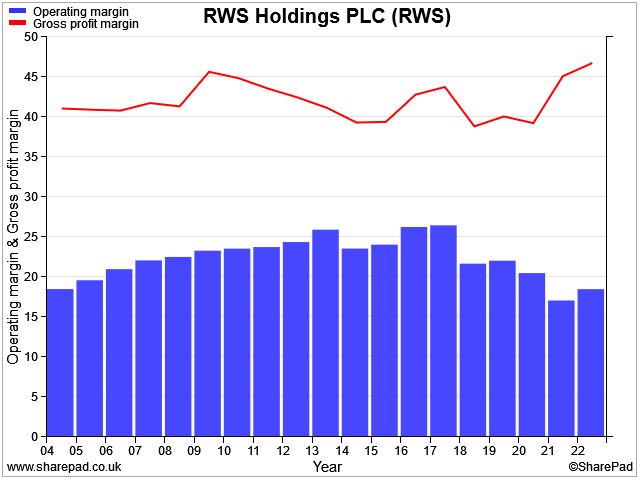

Profitability: disappointing

RWS's growth has come at a price. The company's profitability has worsened steadily over the last 20 years. When I say this, I'm not talking about profit margins (profit as a percentage of revenue). These have remained fairly stable:

However, my experience is that margins don't provide a full picture of a company's long-term profitability.

What I'm looking for is evidence that the business has been able to generate attractive returns while continuing to expand its asset base. This combination can drive attractive long-term compound returns.

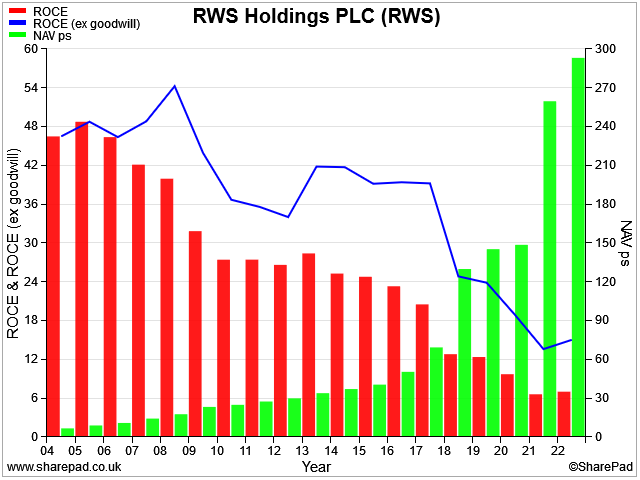

To this end, the factors I use to score for profitability are return on capital employed (ROCE) and net asset value per share:

We can see that ROCE (red bars) used to be exceptionally high – over 40% – but has now declined to single-digit levels.

One reason for this is the company's acquisitive growth. This usually results in a buildup of goodwill on the balance sheet. Goodwill represents the takeover premium, or the price paid on top of the acquired company's asset value.

To illustrate this point, I've also shown ROCE excluding goodwill assets on the chart above. It's higher, but the downward trend is still the same.

We can see that the big acquisitions in 2017 and 2020 generated a step up in RWS's net asset value but caused ROCE to fall.

Over time, this situation may reverse, as the goodwill charge is gradually amortised and new growth projects deliver. In a presentation last year, management said they would target ROCE of 14%-16% from 2024 onwards.

Such an increase could deliver a sharp rise in profit. For now, though, I have to conclude that RWS's profitability is slightly lower than I'd like to see.

RWS scores 2.4/5 for profitability in my screening system.

Fundamental health: a clean sheet

My fundamental health score is really about looking for potential problems relating to debt. I don't see any here, based on the two measures I use:

- Fixed charge cover: EBIT dividend by rent and interest costs

- Leverage, which I calculate as net debt divided by five-year average net profit

Unsurprisingly, RWS earns a perfect score for fundamental health. When paired with the evidence of strong free cash flow I've seen elsewhere in this review, I'm very happy that this business has strong financial footings.

RWS scores 5/5 for fundamental health in my screening system.

Conclusions: in the running

My quality dividend system awards RWS Holdings an overall score of 72/100 at the time of writing (August 2023).

My view: I'd like to spend a little more time on RWS, reviewing some of its larger acquisitions and trying to gauge whether they've delivered value.

However, my initial impressions are quite positive. Here's a summary of the main bull and bear points, as I see them.

Pros:

- RWS has a decent growth record and has increased its dividend for 19 consecutive years

- Cash generation is consistently good and the balance sheet looks strong to me

- Owner management with strong alignment to shareholders' interests.

- The shares could be cheap

Cons:

- The near-term macro outlook is weak, with slower spending and pricing under pressure

- Profitability has suffered as the business has grown

- Over the medium-long term, RWS's business model could be upended and devalued by AI translation systems.

- Regular acquisitions also may carry some risk, especially given the reduction in profitability seen in recent years

On balance, I think RWS has many of the characteristics I'm looking for. I haven't seen anything yet that would cause me to rule out the stock as a possible investment.

I'm keeping RWS on my shortlist as a possible replacement for EMIS.

As always, please let me know what you think in the comments below. Am I being dangerously naive about the likely impact of AI, or is RWS a potential contrarian bargain?

Disclosure: at the time of publication, Roland owned shares in EMIS Group.

Disclaimer: This is a personal blog/newsletter and I am not a financial adviser. All content is provided for information and educational purposes only. Nothing I say should be interpreted as investing advice or recommendations.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.