Is TP ICAP's 8% dividend yield a bargain income buy?

FTSE 250 interdealer broker TP ICAP (LON: TCAP) offers an 8% yield that looks well supported to me. Should I add this high yielder to my dividend portfolio?

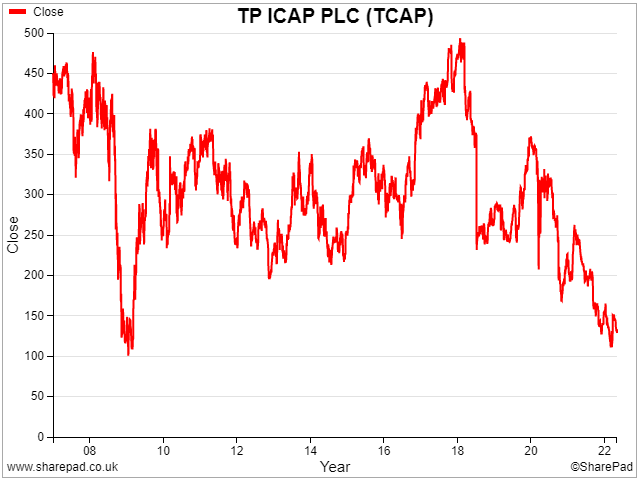

I don't think there are many financial stocks that are as unloved today as FTSE 250 interdealer broker TP ICAP (LON: TCAP).

This City business has seen its share price fall by nearly 75% since 2018.

This painful decline has left this former high flyer offering a forecast dividend yield of 8%, with the potential for a return to growth in 2023.

Assuming we're not heading for another 2008-style financial crisis, then I can only see a couple of likely explanations for TP ICAP's share price slump.

One is that this business is priced for obsolescence and terminal decline. That's a possibility, as I'll explain.

The other possible explanation is that the share price is wrong. Perhaps TP ICAP's brokerage services are still relevant and the business will return to growth.

For the avoidance of doubt, TP ICAP is not a member of my quality dividend model portfolio. However, I'm wondering if I should be paying more attention to this unloved high yielder.

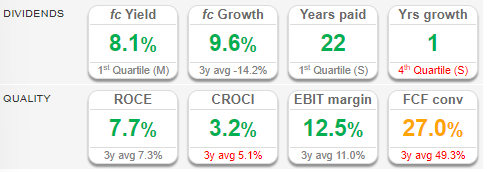

SharePad's summary page presents mixed messages, suggesting some attractive value metrics but a poor record of growth and cash conversion.

To find out more, I'm going to take a look at the stock through the lens of my dividend screening system. I want to find out if I should be considering this business for my quality dividend portfolio.

After all, current forecasts suggest the shares could offer an 8% yield, covered twice by earnings. As an income investor, these are the kind of metrics that get me hot under the collar.

What does TP ICAP do? (and what's wrong)

TP ICAP's core business is Tullett Prebon, a London brokerage firm whose history can be traced back (with many twists and turns) to 1866. You can read about the history of this storied business here.

For my purposes today, I'm going to start the story in 2006, when Tullett Prebon was demerged from stockbroker Collins Stewart and floated on the LSE. At that time, Tullett Prebon was led by CEO Terry Smith (of Fundsmith fame) and was one of the world's largest interdealer brokers.

The company's main selling point was its team of telephone brokers, who would negotiate and arrange transactions between other brokers and market participants (hence, interdealer broker). These were typically non-standard deals that couldn't be handled electronically or on exchanges.

It doesn't take much imagination to guess that demand for such services has dwindled in the 16 years since Tullett's flotation. The number of markets accessible through electronic trading has grown, supported by the data and analytics needed to accurately price more complex transactions.

Terry Smith's departure from Tullett Prebon in 2014 was ostensibly to run his Fundsmith fund management business full time. But I suspect Smith saw the writing on the wall and guessed that voice brokers' best days were behind them.

Smith's successors at Tullett have had little choice but to pursue a strategy of consolidation and diversification. In 2015, Tullett acquired its main London-listed rival ICAP, creating TP ICAP. Other deals have followed, including oil broker PVM and most recently, Liquidnet.

At the same time, TP ICAP has been steadily working to transform its core broking services from "high touch to more profitable low touch channels", to quote CEO Nicolas Breteau.

What this means in practice is shifting as much broking activity as possible onto TP ICAP's new Fusion electronic trading platform, while developing supporting data and analytics services. Today the company bills itself as "a leading electronic market infrastructure and information provider".

Clients will eventually be able to logon directly to Fusion. Mr Breteau's ambition appears to be to gradually squeeze out its expensive human brokers:

By implementing Fusion, we aim to progressively shift the profile of our broking activity from high touch (i.e. a high level of broker involvement in completing a transaction) to low touch (i.e. fully or mostly electronic execution workflow) channels, thereby improving operating margins.

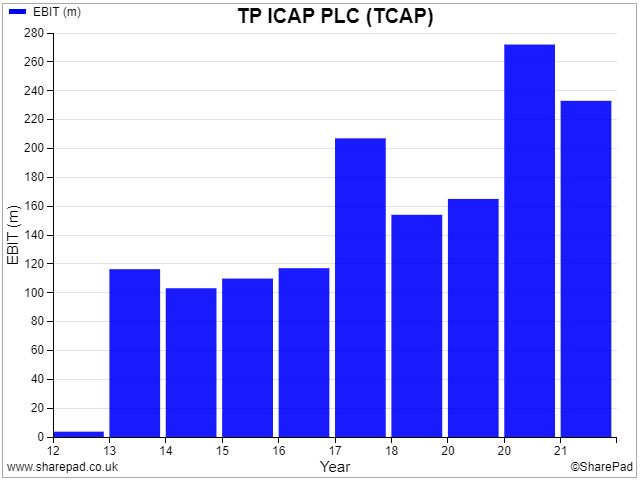

The group's efforts so far have not been entirely in vain. TP ICAP's revenue has risen from £851m in 2012 to £1,865m in 2021. Operating profit has also trended higher over the same period:

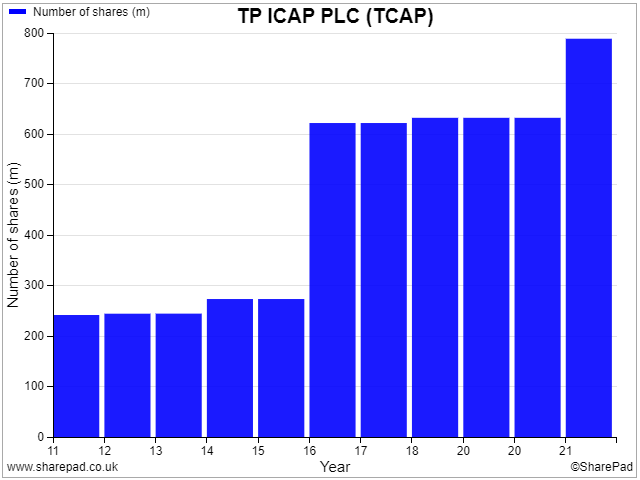

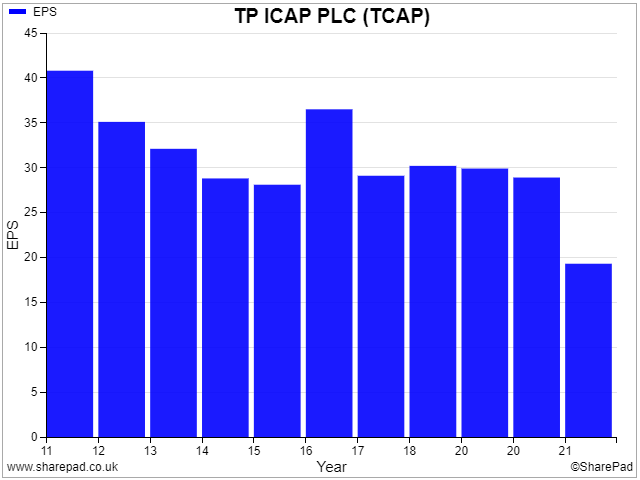

Unfortunately, the group's acquisition spree has resulted in significant dilution. TP ICAP's share count has tripled from 244m in 2012, to 789m today.

This dilution has had an unfortunate effect on earnings per share, which have halved since 2011:

I think it's fair to say that long-term shareholders have not yet had their patience rewarded.

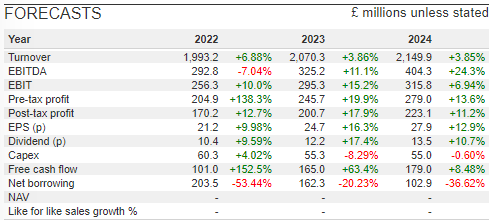

However, investment is about the future, not just the past. TP ICAP shares are now trading on six times earnings and appear to offer a well-covered 8% dividend yield. I don't think too much improvement would be needed to trigger a re-rating of this stock.

TP ICAP: crunching the numbers

Description: Interdealer broker group operating across financial, energy and commodity markets. Combines voice brokerage with data-driven electronic services.

| TP ICAP (LON: TCAP) |

Quality Dividend score: 51/100 | Forecast yield: 8% |

| Share price: 129p | Market cap: £1,050m | All data at 4 May 2022 |

Latest accounts: 2021 final results (15/03/2022)

In the remainder of this review, I'll step through the different stages in my dividend screening system to explain how TP ICAP scores. Unless specified otherwise, the financial data I use in this process is drawn from SharePad.

As a reminder, I use slightly different screening rules for financial stocks. I'll try and highlights these differences as I go, but I covered this topic more fully in this recent piece on Direct Line (disc: I hold).

Dividend culture: Quite strong

TP ICAP has always been a dividend stock, and the company's record in this respect is quite strong.

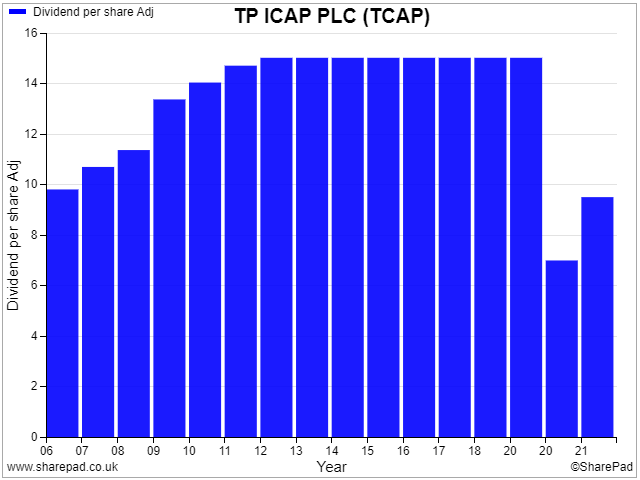

Until the pandemic intervened, TP ICAP's dividend per share had not been cut since since the Tullett Prebon business was spun out of Collins Stewart at the end of 2006:

Although the payout was flat from 2012 until 2020, we've already seen that the share count rose sharply during this period. So the total payout increased substantially.

My dividend culture score only looks at continuity of payments and ignores any cuts. That means TP ICAP scores quite highly in this category.

TP ICAP scores 4/5 for dividend culture in my screening system.

Dividend safety: not too bad

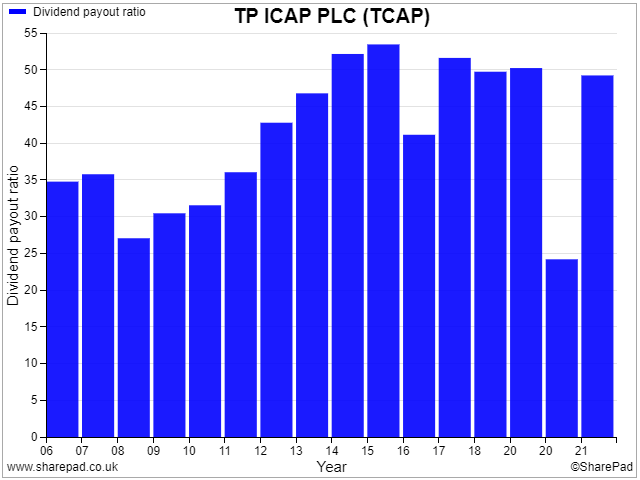

My dividend safety score looks at a company's historical and recent dividend payout ratio.

I do this to try and spot companies which might be distributing too much of their earnings to shareholders, leaving too little to strengthen or expand their businesses.

According to SharePad, TP ICAP's dividend payout ratio has averaged around 45% for most of the last decade, with a couple of blips:

TP ICAP's current dividend policy is to maintain a payout ratio of 50% of adjusted earnings. This seems reasonable to me. I don't have any concerns in this area.

TP ICAP scores 3/5 for dividend safety in my screening system.

Dividend growth: weak

The purpose of my dividend growth score is to test the sustainability of a company's dividend growth. This score has two elements:

- 5yr average dividend growth

- 5yr average net asset value per share growth

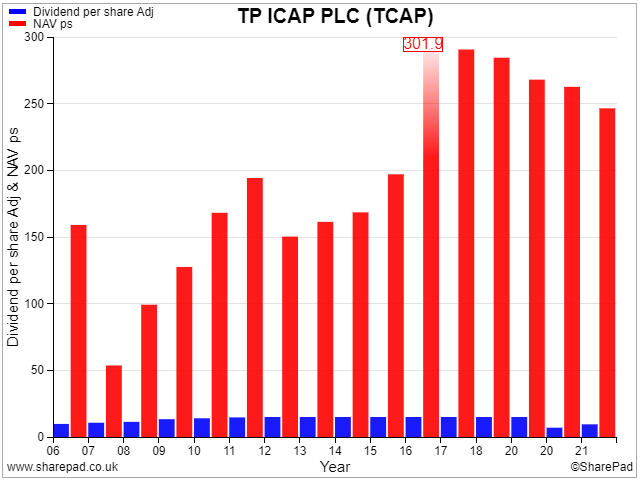

The purpose of this is to test whether a company is maintaining dividend growth by slowly liquidating its assets. That scenario would likely be reflected in a falling NAVps.

Here, my scoring system provides a rare negative score. TP ICAP's NAVps and its dividend have both fallen over the last five years:

However, I would probably argue that the stock's falling NAVps is the result of changes relating to the acquisitions and equity raises that have taken place over the last year.

For example, net asset value rose from £1.7bn to £2.0bn last year, but NAV per share fell because of the increased sharecount.

On balance, I'm not overly concerned about TP ICAP's falling NAVps, as long as this decline levels out in 2022.

TP ICAP scores -0.5/5 for dividend growth in my screening system.

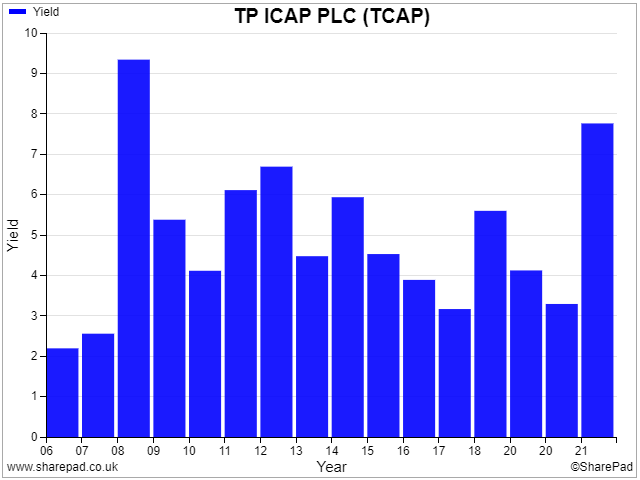

Dividend yield: high

With a forecast dividend yield of 8% you would probably expect TP ICAP to score highly for yield. It does, but I don't just look at forecast yield.

My scoring algorithm blends together forecast yield, five-year average yield and TTM yield to gain a more rounded view on the stock's typical yield.

TP ICAP has been a high yield stock for most of its time as a listed business, but we can see from this chart that the yield is unusually high at the moment:

In general, I would see such a high yield as a sign of either value or distress. In this case, I think it's more likely to indicate value.

TP ICAP scores 4/5 for dividend yield in my screening system.

Profitability: middling

One of the main aims of my system is to build a portfolio of stocks with above-average profitability.

In some ways I think this is more important than dividend yield. The reason for this is that I aim to hold my stocks for many years. If they are not profitable enough to compound faster than the market average, then I suspect I'm likely to underperform over time.

On the other hand, highly profitable businesses with good cash conversion should naturally generate higher dividends over time, improving the income from my portfolio.

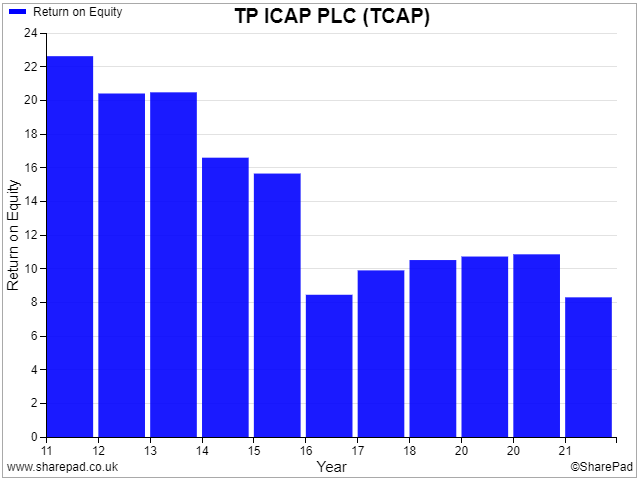

For financial stocks, I use two measures of profitability:

- 5yr average return on equity

- TTM return on equity

We can see that TP ICAP's return on equity has been pretty humdrum since 2016, according to SharePad. This reflects the big increase in intangible assets which followed the merger with ICAP:

Some people might adjust out these intangibles, but I prefer not to. They represent real capital deployed by management, so I think it's right to measure returns against them.

Overall, it's a rather mixed picture. But if the TP ICAP's turnaround gathers pace and profitability improves as promised, I would expect ROE to rise.

TP ICAP scores 3/5 for profitability in my screening system.

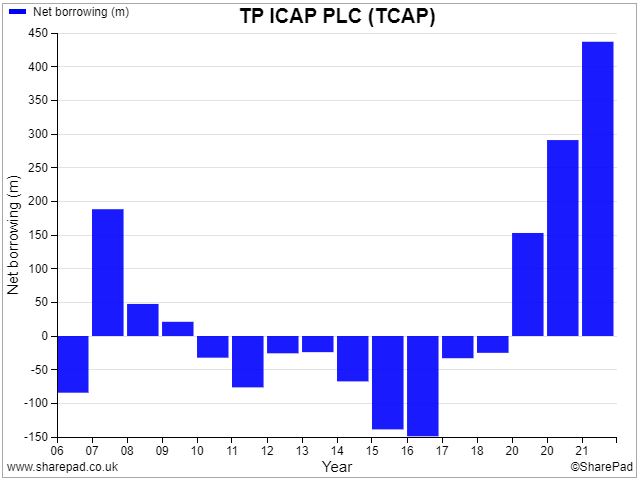

Leverage: moderate

TP ICAP's borrowing has steadily increased over the last decade, presumably due to the company's long-running cycle of acquisitions and restructuring.

I calculate financial net debt at £166m, or £435m including IFRS 16 lease liabilities. This matches up with SharePad's numbers:

I don't generally use net debt as a metric for financial stocks. It's not always relevant or even easily calculable. However, I think it is useful in this case.

Converting net debt into leverage tells me that TP ICAP's net debt is around three times last year's adjusted net profit. That's within the range I allow when screening non-financial stocks.

My normal leverage metric for financial stocks is based on the ratio of assets to equity. As I discussed in my review of Legal & General (disc: I hold), I'm reviewing this approach, as I don't think it's suitable for life insurers, in particular.

In this case, I think it might give me some useful information. Or at least it might do if TP ICAP's balance sheet had not been transformed by the impact of acquisitions and rights issues.

My judgement, based on a review of TP ICAP's borrowings, is that the group's leverage is moderate and not a concern. But once again, I feel my scoring system is not up to the job of interpreting this balance sheet accurately.

For what it's worth, TP ICAP scores 2/5 for leverage in my screening system.

I think this judgement may be harsh, but I think it's better to be conservative in such a changing business.

Conclusion: a turnaround buy?

TP ICAP scores a 51/100 in my dividend screening system at the time of writing (May 2022).

This is one of the lowest scores of any qualifying stock.

TP ICAP's inconsistent track record will probably prevent me from adding the shares to my quality dividend model portfolio.

But if I was still in the habit of investing in value and turnaround stocks, then I'd be very tempted to buy some shares in TP ICAP.

CEO Nicolas Breteau appears to be steadying the ship and I think that TP ICAP's scale and client networks are likely to remain valuable. It seems reasonable to assume that the group's financial performance could now start to improve.

The main short-term risk seems to be that market conditions will not favour TP ICAP. Looking further ahead, I wonder if the group could struggle to differentiate its offering as it comes to rely more on data-driven electronic trading.

Stock market history suggests to me that as data becomes more widely available and markets more interconnected, it becomes harder for any proprietary platform to maintain an edge.

Even so, I think TP ICAP looks interesting at current levels.

Disclaimer: This is a personal blog and I am not a financial adviser. All content is provided for information and educational purposes only. Nothing I say should be interpreted as investing advice or recommendations.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.