Quality dividend portfolio: 2022 review

I review the performance of my quality dividend portfolio in 2022, including dividend income, trading activity and comments on the outlook for 2023.

2022 turned out to be an acceptable enough year for my portfolio, although it wasn't always obvious that this would be the case.

Rising interest rates and inflation have led some investors to suggest that a different approach is needed to that which has worked in recent years.

That may be true in some cases, but personally I found the opposite to be true. When dealing with difficult and unfamiliar circumstances, having a clear, systematic process became more valuable than ever for me.

In any case, I try not to read to much into a year's performance. As Richard Beddard noted in his latest SharePad article, "one good or bad year tells us nothing about the skill of an investor".

However, while yearly intervals may be fairly arbitrary, they are still convenient for measuring performance. They tie in with company reporting cycles and have the additional benefit of being widely used, aiding comparability.

In this report:

- 2022 portfolio performance review

- Portfolio changes in 2022 - three new stocks, three takeovers & two unforced errors

- Financial characteristics of the portfolio

- Sector allocation

- Conclusions (thoughts on interest rates)

- 2023 portfolio plans

Portfolio performance

To recap, the portfolio I'm discussing here is my quality dividend model portfolio, which is run using my dividend screening system.

The model portfolio was launched on 1 December 2021, but it contains largely the same shares as my personal portfolio, which has been run on a similar basis for a number of years.

One key difference is that the model portfolio is based on a single lump sum, rather than regular investments. This makes it much simpler to track performance.

With that said, here's how the model portfolio performed in 2022:

- Model portfolio dividend income: 4.6% (based on 31/12/21 share prices)

- Model portfolio total return: -1.0%

- FTSE 100 total return tracker (acc. units): +5%

- FTSE 100 dividend yield: 3.7%

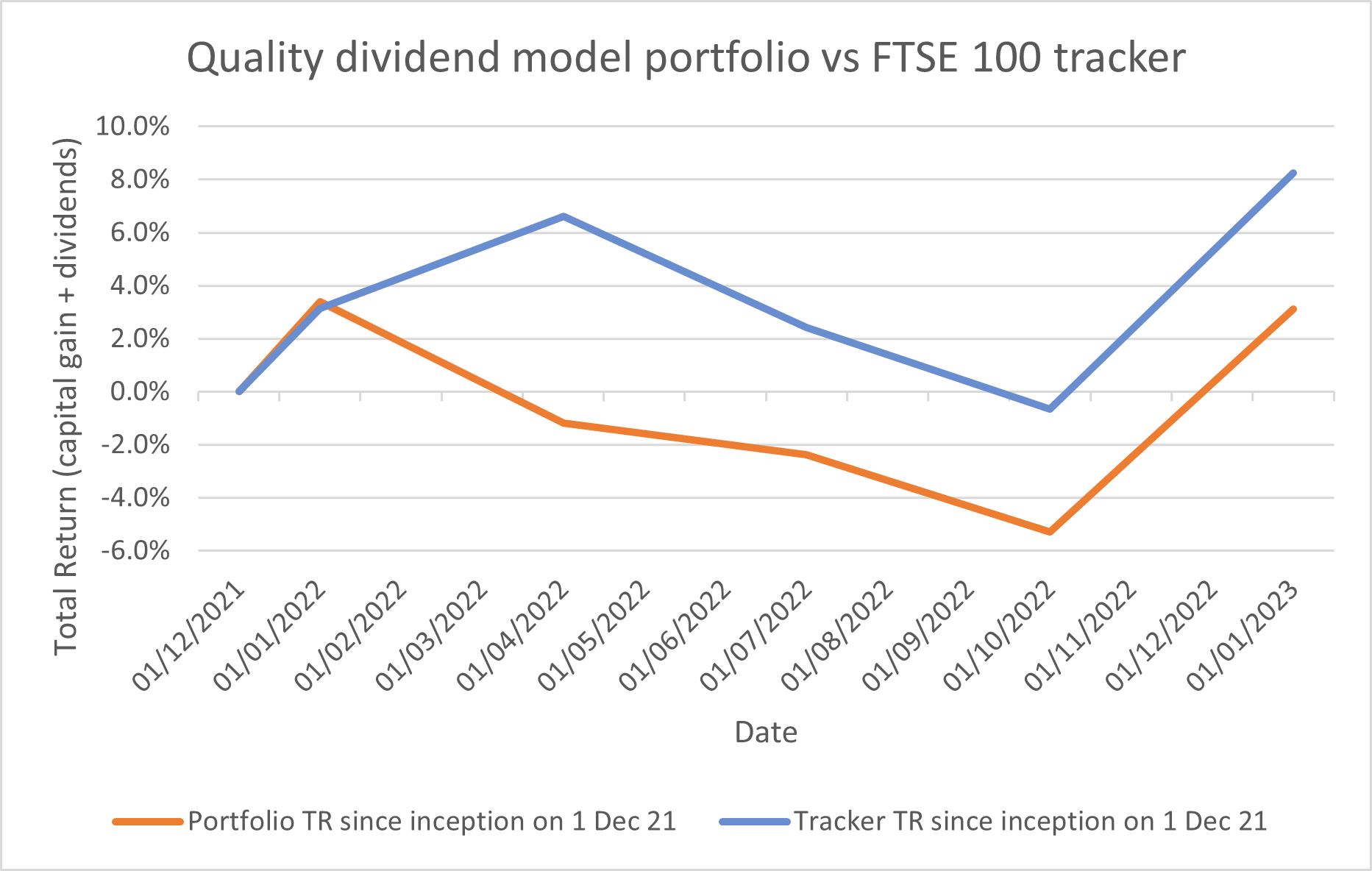

This chart shows the portfolio's performance against its FTSE 100 tracker benchmark since inception (01/Dec/2021). Both lines show total return (capital return + dividends):

The combination of a negative total return and a positive dividend income tells us that the portfolio's capital value fell last year.

On average, the shares in the model dividend portfolio fell by 5.6% in 2022.

This compares to a 20% fall for the FTSE 250 and a 1% gain for the FTSE 100.

This unusual result can be explained by a quick look at the make-up of these indices. The FTSE 100 is a market-cap weighted index, which means the largest companies have the biggest impact on the value of the index.

The events of last year saw some of the FTSE's biggest constituents deliver exceptional gains, propping up the whole index. For example:

- Shell (+43%)

- BAE Systems (+56%)

- BP (+45%)

- Glencore (+47%)

Taking a broader view, more than 70% of FTSE 100 stocks fell last year, as did a similar proportion of FTSE 250 stocks. I don't think private investors who underperformed the FTSE 100 last year should beat themselves up too much.

Portfolio changes in 2022

The portfolio saw more trading than I would have liked or expected in 2022. There were two reasons for this:

- Ukraine

- Takeovers

Stocks sold

Ukraine: the Russian invasion of Ukraine prompted me to recognise two likely mistakes in my portfolio construction. Rather than dwelling on them too long, I sold immediately:

- Gold miner Polymetal International (LON:POLY) - sold at 746.4p for a loss of 45% on 25/Feb/22 (sale report here)

- Copper/zinc group Central Asia Metals (LON:CAML) - sold at 229p for a loss of 6% on 3/Mar/22 (sale report here).

Takeovers: three companies in my portfolio received takeover offers last year:

- Air Partner (LON:AIR) - sold at 122p for a gain of 55% on 25/Feb/22 (sale report here)

- Homeserve (LON:HSV) - sold at 1,172p for a gain of 38% on 30/June/22 (sale report here)

- EMIS Group (LON:EMIS) - not yet sold; sale expected to complete in Q1 2023 (comment here)

Homeserve was added to the portfolio to replace Air Partner, but the home repair specialist received a takeover bid within three months of my purchase. I think this highlights the value that was on offer in the UK market at the time, rather than any particular skill on my part.

I'm a little sad to lose AIR, HSV and (probably) EMIS, as I think they were all good businesses with the potential to deliver the kind of compound growth I'm seeking.

However, I can't really complain. Takeovers are part of the game, and these quick profits helped to offset the portfolio's unfortunate early loss on Polymetal International.

New stocks

During 2022, I added three new stocks to the portfolio to replace Polymetal International, CAML, Air Partner, and then Homeserve. Here are the links to my buy reports on each stock (subscribers only):

- Portfolio shares: adding US exposure to the portfolio (bought 1 April 2022)

- Portfolio shares: a 170-year-old business to replace Homeserve (bought 1 July 2022)

- Portfolio shares: a cyclical FTSE 250 stock with a 6%+ yield (bought 1 October 2022)

I added each stock to the portfolio on the first day of the new quarter, in line with my trading policy of only allowing myself a maximum of two trades each quarter.

Financial characteristics of the portfolio

The perfect stock probably doesn't exist. Like the businesses from which they derive, most stocks are stronger in some areas and weaker in others.

For example, some of the companies in my portfolio have higher yields and lower growth rates. For others, it's the opposite.

I'm quite content with this. While the selection of individual stocks can be exciting and rewarding, what really matters is the performance of the overall portfolio.

For this reason, one of the techniques I use to monitor the quality and expected performance of my portfolio is to calculate average financial metrics for all of my stocks.

This allows me to get a feel for the overall shape of the portfolio, and monitor whether it's likely to be improving or worsening.

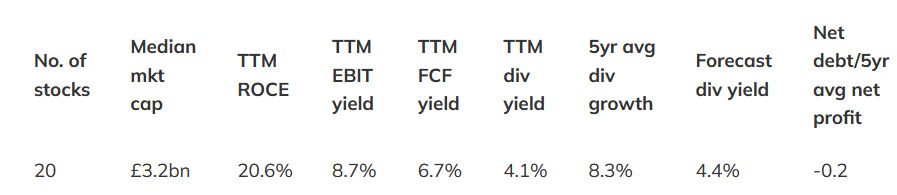

Here's are the performance metrics for the portfolio at the end of 2022:

| Median mkt cap | TTM ROCE | TTM EBIT yield | TTM FCF yield | Net debt/5yr avg net profit | TTM div yield | 5yr avg div grth | F'cast div yield | No. yrs div paid |

| £2.3bn | 22.2% | 9.4% | 7.0% | 0.3x | 4.5% | 7.6% | 5.0% | 21 |

Data source: SharePad/author analysis 03/01/2023. Some adjustments were needed - don't take this as gospel.

The portfolio average ROCE of 22% tells me that in aggregate, at least, my companies are far more profitable than average.

The trailing 12-month EBIT (earnings before interest and tax) and FCF (free cash flow) figures suggest that the portfolio is quite reasonably valued. These numbers also tell me that in aggregate, my companies convert around 75% of their operating profit into free cash flow. That's a good performance, in my view.

One reason for this healthy cash conversion is that these companies don't have to spend too much on interest payments (which are deducted from EBIT). Average net debt across the portfolio is just 0.3x five-year average net profit.

Looking ahead, the trailing dividend yield of 4.5% and forecast dividend yield of 5% imply aggregate dividend growth of 11% this year. I expect the final result to be slightly different to this, probably lower, but this estimate is in the same ballpark as the five-year average dividend growth of 7.6%.

Finally, the portfolio's trailing free cash flow yield of 7% tells me that the trailing dividend yield of 4.5% was covered comfortably by free cash flow, at least in aggregate.

How did it change in 2022? Market conditions and the make-up of the portfolio have changed significantly over the last year. How do these numbers compare with the picture at the start of 2022?

Pleasingly, they're very similar:

Of course, this attractive aggregate profile does not mean that all the stocks in the portfolio are potentially attractive buys. Averages can be used to mask a multitude of sins. For example, cash cows with limited growth potential might be masking over-valued growth stocks with poor cash generation.

There's always a risk. But on balance, I'm happy that the portfolio has stayed on track after a difficult and unusual year.

Sector allocation

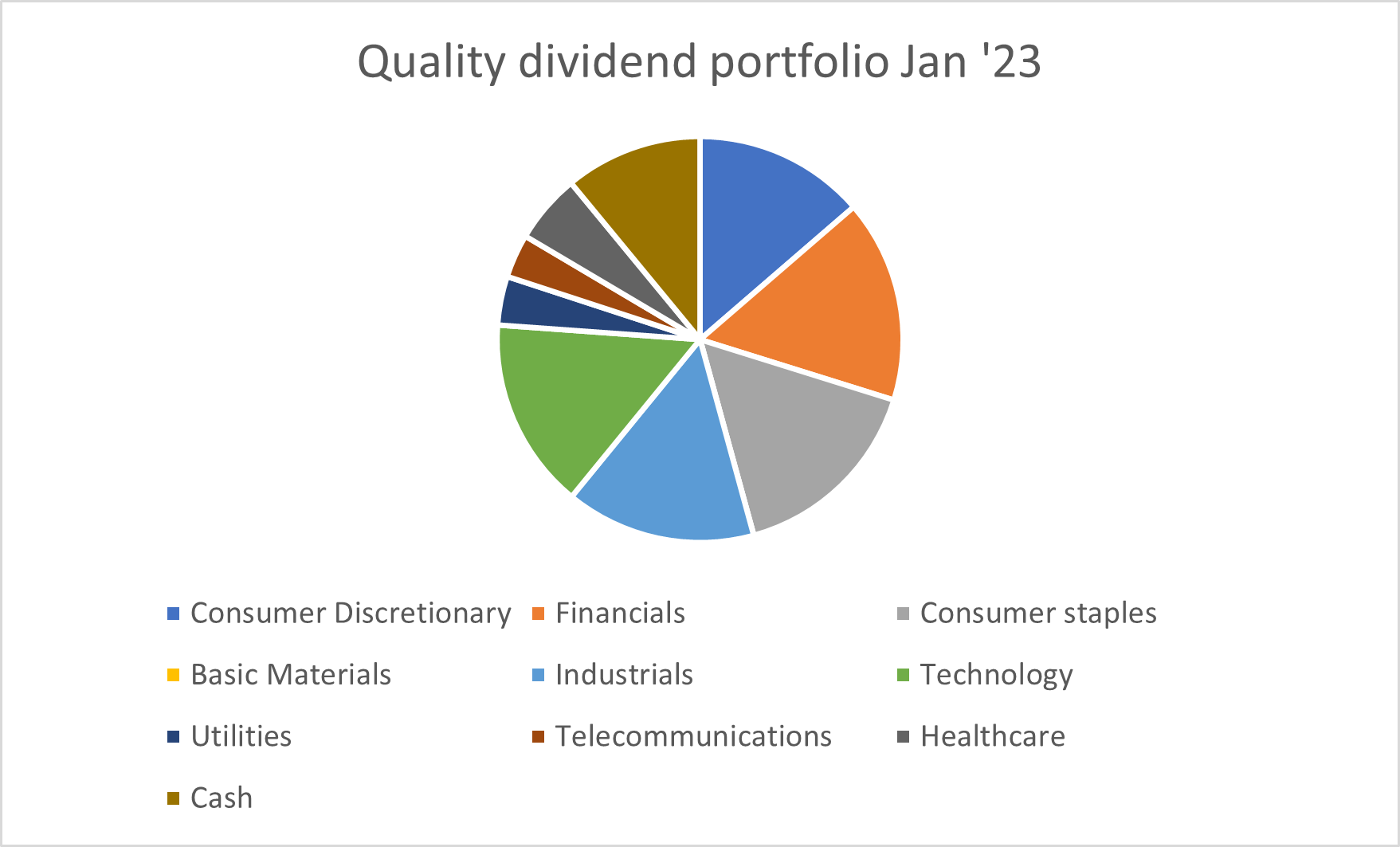

My intention is always to maintain a reasonable degree of sector diversification. But equally, this is a dividend portfolio; I have to go where the income is.

In the UK market at least, some sectors offer significantly more income potential than others. Here's how the portfolio was weighted at the start of 2023:

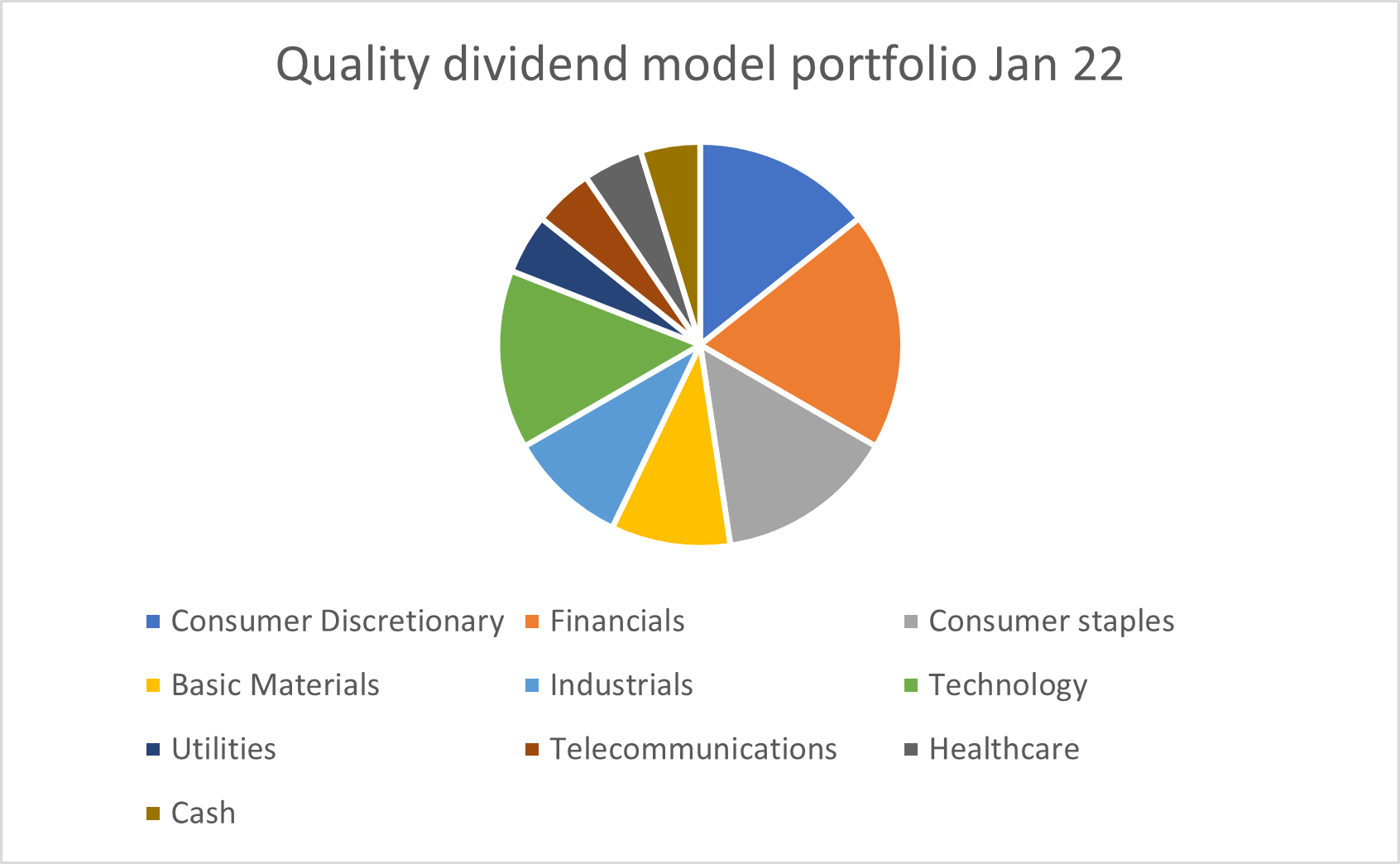

Here's how this chart looked one year ago (Jan '22):

The model portfolio's growing cash balance is a result of dividend income. This will need to be reinvested. I'll cover this topic over the coming months.

Conclusions

Don't ignore rising interest rates

The war in Ukraine appears to have blown the starting whistle on a long-awaited bout of inflation and rising interest rates. UK inflation has topped 10%, while the Bank of England Base Rate has risen from 0.1% to 3.5% in the space of one year.

Interest rates and inflation both had a notable impact on markets in 2022. I try to avoid macro forecasts, but I think this disruption is likely to continue into 2023.

Highly-rated US tech stocks and cryptocurrencies have been most dramatically hit by the end of the cheap money era. But even for investors with a focus on more defensive, quality businesses, I think the impact of rising interest rates is worth considering.

Interestingly, famed investor and Fundsmith founder Terry Smith flagged interest rates as a key risk to his portfolio back in 2019.

Maynard Paton and Mark Atkinson recently took a closer look at this issue and at the outlook for Fundsmith in the Private Investor's Podcast – which I'd recommend – but to explain why Smith might bave been worried, here's a simple example.

FTSE 100 drinks group Diageo has an investment grade credit rating and is generally viewed as a safe, defensive business. In October 2022, Diageo issued $2bn of bonds with coupon (interest) rates between 5.2% (three year) and 5.5% (10 year).

Less than three years ago, in April 2020, Diageo was able to borrow the same kind of money at rates ranging from 1.375% (five year) to 2.125% (12 year).

Corporate bond rates have eased slightly since October, I think. But it seems reasonable to assume that this high-quality business may now have to pay 3% more to borrow money than it did three years ago.

That's a staggering difference.

Based on a net debt figure of £14bn, my sums suggest this increase in borrowing costs could lead to an increase of £420m in Diageo's annual interest bill. That's almost double the company's 2022 interest bill of £438m, and would represent nearly 10% of last year's £4.4bn operating profit.

This increase in interest costs won't be felt immediately. Most big companies maintain a portfolio of debt that rolls over gradually, a little each year.

I'd guess that we might see Diageo's interest bill rise steadily over the next three to six years, perhaps – unless management divert more of the group's free cash flow to debt repayments.

If the company does opt to reduce leverage, then that might mean reduced investment in growth – or even a dividend cut. I think the latter is unlikely at Diageo, but it could certainly happen at weaker businesses.

Indeed, I think the impact of higher interest rates on some businesses may be quite sudden and severe.

More than ever, I think this is a good time to be focusing on companies with modest leverage or net cash positions.

2023 portfolio plans

I expect to add one new stock to the portfolio when the EMIS takeover completes. This has been delayed, but the company now expects to seal the deal by the end of March.

I'm not planning any changes to my investment strategy, although I am working on some small refinements to my scoring system. I'll detail them here if this takes place, but I'm wary of the risk of trying to narrow the funnel too much.

I use the screen to create a manageable menu of stocks to consider, not as an automated selection tool. So I'm happy to do some manual filtering, too, rather than risking ruling out too many potential candidates.

More generally, I'm hoping to invest more time in this website in order to make some technical improvements and add more UK dividend stock coverage. Watch this space.

I'll explain any changes here as they happen. In the meantime, please feel free to contact me through Twitter or by email if you have any questions.

For now, all that remains is for me to thank you for your continued support and wish you good luck in the markets in 2023.

I look forward to your feedback and will be adding a comment facility to this site very shortly (!). In the meantime, you can always reach me on Twitter @rolandhead or by email.

Disclaimer: My comments represent my views only. I am not a financial adviser. The information provided is for information and interest. Nothing I say should be construed as investing advice or recommendations. The investing approach I discuss relates to the system I use to manage my personal portfolio. It is not intended to be suitable for anyone else.

You should carry out your own research and make your own investing decisions. Investors who are not able to do this should seek qualified financial advice. Reasonable efforts are made to ensure that information provided is correct at the time of publication, but no guarantee is implied or provided. Information can change at any time and past articles are not updated.